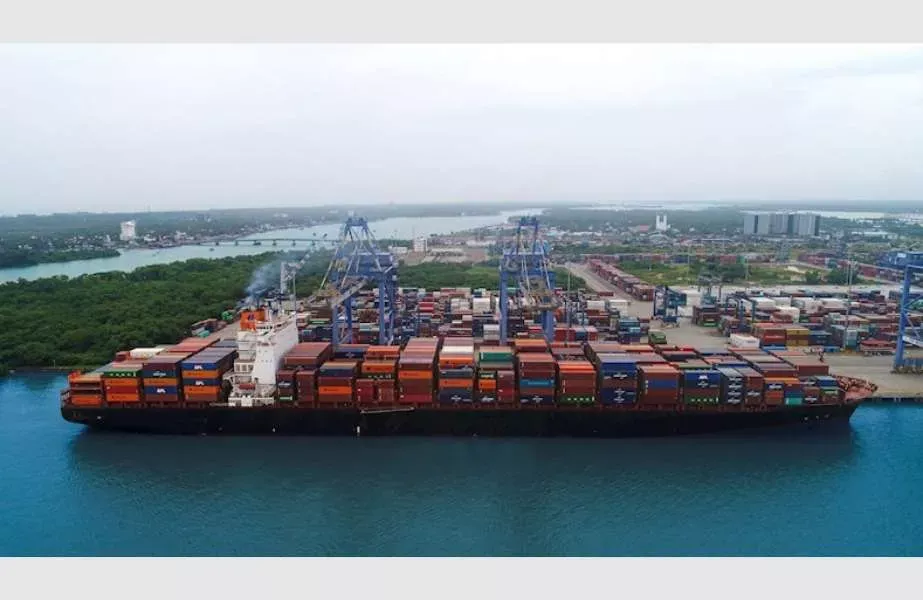

The sustained growth in maritime throughput across regional logistics hubs signals a structural realignment of trade flows that MENA economies must actively arbitrage to preserve their transit dominance. Traditional port models optimized solely for vessel calls and crude tonnage are being rapidly decommissioned in favor of digitally integrated, multimodal trade corridors that prioritize cargo velocity and value-added processing over raw volume. For regional operators, the business imperative has shifted toward embedding autonomous terminal systems, predictive customs clearance, and cross-jurisdictional supply chain visibility. This transition is not merely operational; it is a strategic repositioning designed to capture higher-margin logistics activity amid the ongoing fragmentation of global shipping routes and the rerouting of Indo-African-Eurasian maritime freight through Gulf and North African gateways.

Sovereign capital allocations are evolving to de-risk the capital-intensive nature of next-generation port infrastructure through syndicated equity structures and performance-linked concession frameworks. State-backed funds across the GCC and Levant are increasingly pairing heavy civil engineering spend with strategic investments in logistics fintech, cold-chain automation, and trade data platforms, recognizing that physical capacity without digital integration yields rapidly diminishing marginal returns. This sovereign pivot is actively shaping regional venture capital deployment, with institutional family offices and dedicated deep-tech funds directing significant late-stage and growth equity toward AI-driven port optimization, blockchain-backed bill of lading settlement, and predictive inventory management. The convergence of patient state capital and agile venture deployment is forging a unified financing stack that compresses scaling cycles and ensures infrastructure projects achieve commercial viability without relying on perpetual subsidy mechanisms.

The macroeconomic implications for MENA extend well beyond terminal expansion, directly impacting foreign direct investment retention, non-hydrocarbon GDP diversification, and regional manufacturing competitiveness. By aligning upgraded port infrastructure with harmonized customs protocols, special economic zones, and digitized trade finance rails, Gulf and North African states are engineering defensible moats against competing Asian and Mediterranean hubs. The velocity at which these nodes clear cargo, settle cross-border transactions, and integrate with regional free trade agreements will dictate capital allocation flows over the next decade. Ultimately, sustained market leadership will depend not on static berthing capacity, but on the strategic deployment of sovereign-backed digital infrastructure and venture-backed logistics innovation to anchor long-term, export-oriented industrial ecosystems across the region.