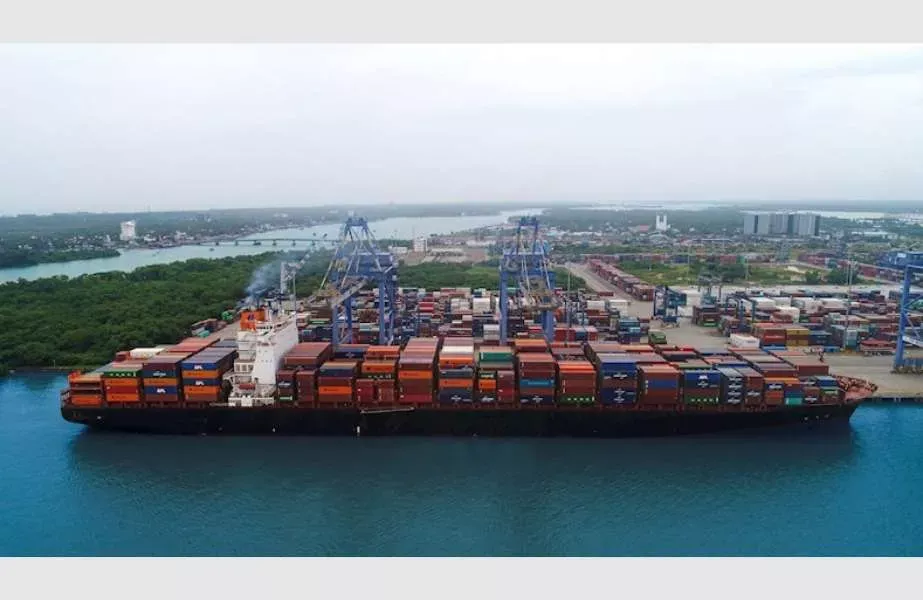

The recentwave of Iranian drone and missile incursions targeted critical petrochemical complexes, port facilities, and power‑desalination installations across the Gulf, forcing immediate operational halts at sites such as Ruwais, Borouge, and the Habshan gas complex. While casualties remain limited, the incidents have precipitated costly production suspensions, accelerated damage assessments, and triggered emergency maintenance cycles that will compress first‑quarter earnings for both state‑controlled and privately held energy operators. The swift containment of fires underscores the effectiveness of indigenous air‑defence systems, yet the frequency of such attacks is likely to elevate insurance premiums and necessitate additional capital allocations for redundancy and hardened infrastructure.

From a sovereign‑capital perspective, the sustained threat environment introduces a measurable risk premium on Gulf sovereign debt and sovereign‑wealth fund portfolios exposed to energy assets. Rating agencies are expected to factor heightened security costs into fiscal outlooks for the UAE, Saudi Arabia, and Kuwait, potentially tightening sovereign borrowing spreads. Governments may re‑prioritise budgetary resources toward defence Modernisation and infrastructure hardening, diverting funds that would otherwise support diversification initiatives and social programmes, thereby influencing long‑term fiscal sustainability metrics.

For venture capital and private‑equity investors, the crisis reinforces a risk‑averse stance toward early‑stage deals in sectors directly linked to vulnerable energy assets, while simultaneously spurring demand for resilience‑focused technologies—advanced monitoring, AI‑driven threat detection, and modular plant designs. Limited partners are likely to demand higher hurdle rates for Gulf‑based funds, yet opportunities will emerge in cybersecurity, modular petrochemical recovery systems, and decentralised water‑treatment solutions, sectors poised to attract strategic allocations from both regional sovereign investors and global VC networks.

On a macro‑regional level, recurring attacks on civilian infrastructure are accelerating a strategic shift toward integrated defence‑logistics architectures and the diversification of export routes away from traditional chokepoints. Gulf states are expected to deepen cross‑border coordination on maritime security and invest in hardened supply‑chain nodes, which will reshape long‑term energy logistics planning and influence multinational infrastructure financing decisions. The confluence of heightened security externalities with sovereign capital reallocation will likely catalyse a more cautious, yet technologically sophisticated, approach to regional energy and water system investments.