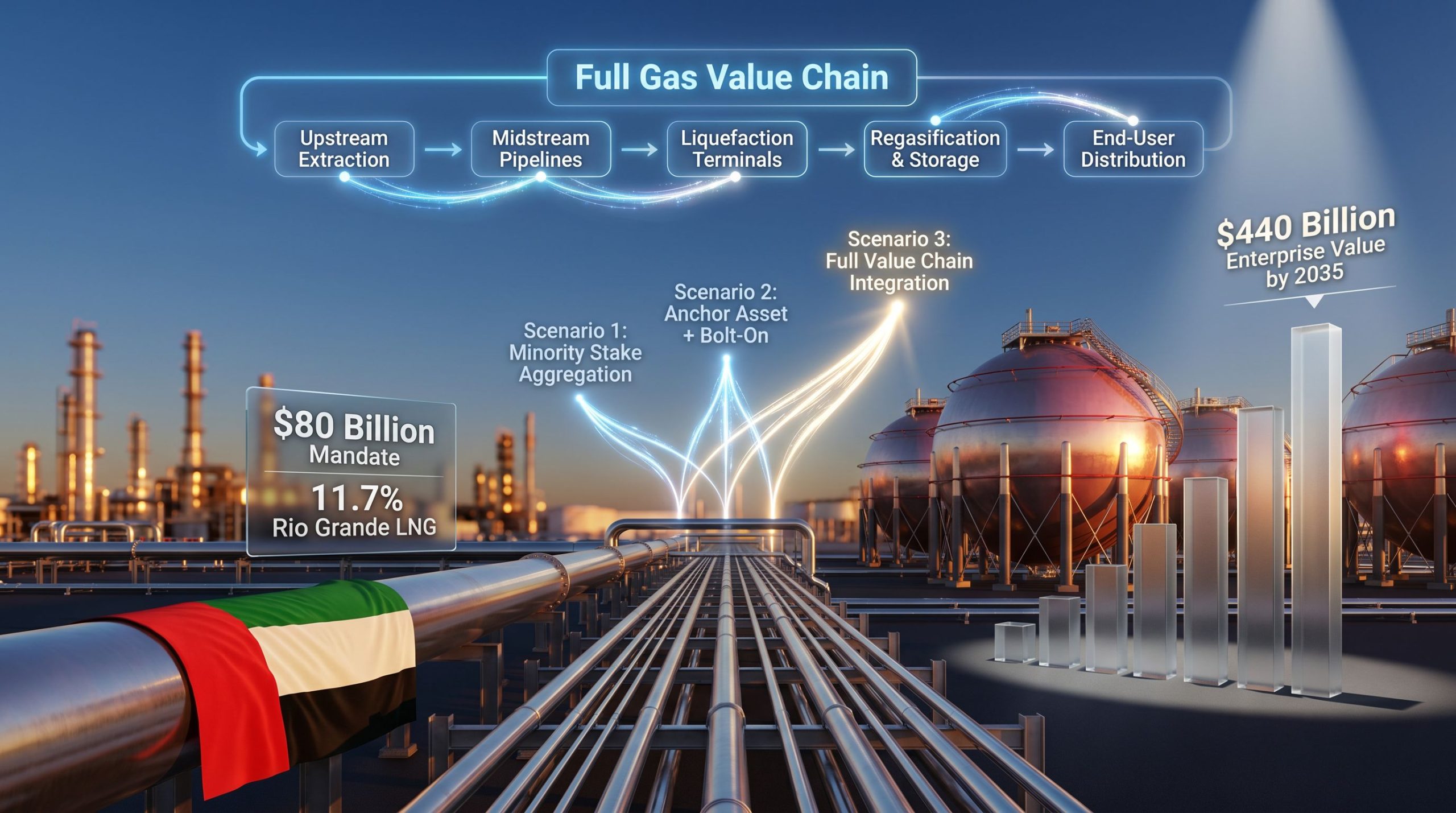

The recalibration of Abu Dhabi’s capital deployment strategy through XRG marks a structural departure from rentier commodity models toward the architectural control of integrated gas systems. By targeting vertical consolidation across United States upstream basins, regulated midstream corridors, liquefaction export nodes and destination-market regasification infrastructure, Abu Dhabi National Oil Company is engineering exposure to margin capture rather than mere volumetric lift. The $80 billion mandate functions as a balance-sheet bridge between sovereign hydrocarbon cash flows and a trans-Atlantic industrial platform, converting commodity cycle volatility into balance-sheet optionality. For MENA sovereign wealth and national oil companies, the move signals that strategic insulation from price risk now requires ownership of chokepoints, not merely access to molecules.

Investment implications for regional capital allocators extend beyond bilateral energy trade into the reconfiguration of global LNG market structure. The United States Gulf Coast has become the critical infrastructure theatre for supply elasticity, offering rule-of-law protections, tariff-based midstream returns and scalable liquefaction capacity that emerging-market sponsors increasingly struggle to replicate domestically. By embedding XRG across the value chain, Abu Dhabi secures feedstock cost control, contracted throughput stability and destination-market pricing leverage while diluting exposure to Asian spot LNG price dislocations. Competing sovereign models—in Qatar and Saudi Arabia—remain predominantly anchored to offtake or downstream stakes; XRG’s multi-node play represents the most aggressive attempt by MENA capital to internalise the economic rent of seaborne gas across a foreign regulatory jurisdiction.

Infrastructure financing and venture capital ecosystems across the Middle East and North Africa will face mounting pressure to syndicate similar cross-border energy platforms or risk capital sidelining. The XRG architecture raises the hurdle for regional LNG export projects seeking sovereign offtake backing, as Gulf balance sheets pivot toward co-investment in proven U.S. regulatory and logistics frameworks rather than greenfield domestic megaprojects with execution risk. Data centre-driven baseload gas demand in North America further de-risks upstream and midstream valuations, creating a rare alignment of strategic buyer conviction and secular demand elasticity. For regional markets, this presages a redirection of petrodollar liquidity into trans-Atlantic midstream yield vehicles and a hollowing-out of capital appetite for higher-risk, unintegrated LNG developments closer to home.