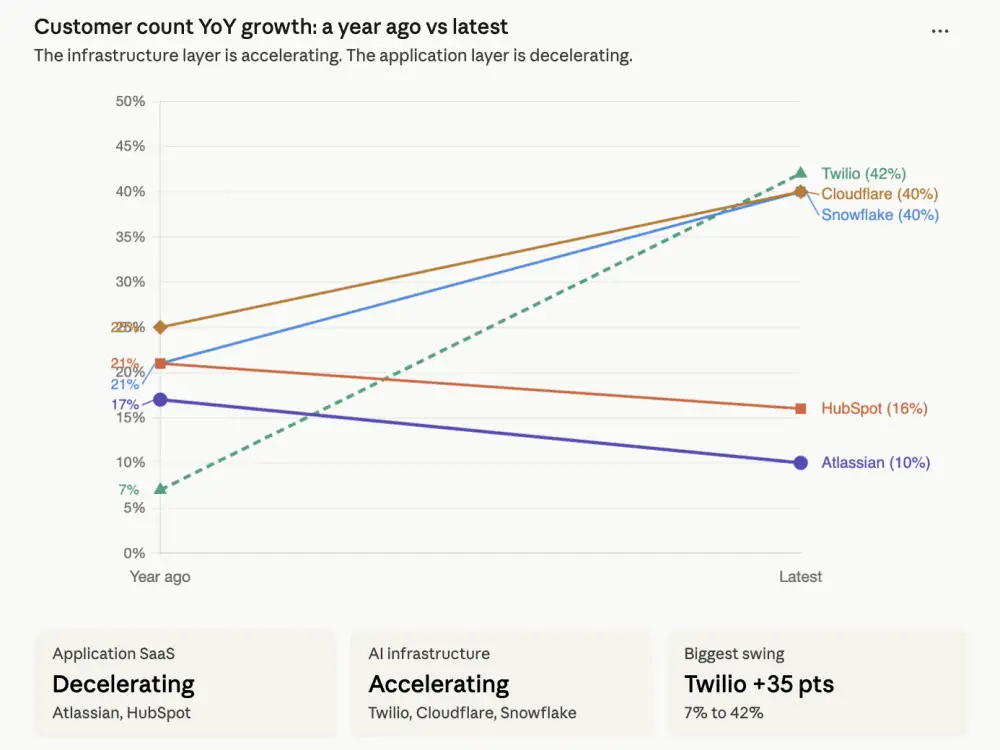

The structural bifurcation now cleaving global B2B markets is materialising with acute force across the Middle East and North Africa, where sovereign capital and venture pools are recalibrating deployment strategies around durable infrastructure demand rather than cyclical application adoption. Net new customer growth—unencumbered by expansion revenue accounting—has become the decisive indicator of commercial optionality, separating platforms that are capturing AI-native formation from incumbents dependent on legacy seat economics. For regional allocators, the imperative is no longer whether capital is available, but whether it is being directed toward substrate-layer infrastructure that compounds customer acquisition at scale. The data reveal that markets rewarding new-logo velocity are tightly coupled to AI build-out; everything else is harvesting.

Sovereign balance sheets and large limited partners are pivoting to back logistics, energy, and data-stack infrastructure capable of absorbing institutional risk over decade-long horizons. The consequence is a marked shift in venture deployment away from late-stage application SaaS toward regional hyperscale enablers—edge networks, data fabrics, and AI orchestration platforms—that exhibit the customer accretion profiles of Cloudflare or Palantir rather than the logo stagnation of Atlassian. Capital recycling within Gulf cooperation councils is accelerating funding for companies that can demonstrate verifiable pipeline formation among AI-centric operators, effectively importing a Silicon Valley–grade infrastructure demand curve into markets where sovereign wealth is underwriting digital capacity expansion. This recalibration compresses multiples for seat-based models while expanding terminal value for platforms that can aggregate high-value enterprise cohorts across fragmented MENA verticals.

Infrastructure implications extend to national digital stacks and pan-regional connectivity corridors, where customer growth rates now determine negotiating leverage with tower, fibre, and compute operators. States underwriting smart-city and logistics-platform roll-outs are prioritising vendors whose customer counts are growing faster than revenue—a signal of durable demand formation—rather than those relying on net revenue retention to mask saturation. Venture firms are mirroring this discipline, using cohort quality as a filter for follow-on liquidity and IPO readiness, particularly in Gulf markets preparing primary listings. For corporates and sovereign allocators alike, the inflection is clear: capital is migrating toward architectures that convert small-account floods into concentrated enterprise ARR, turning the AI infrastructure wedge into the central variable governing regional technology market leadership.