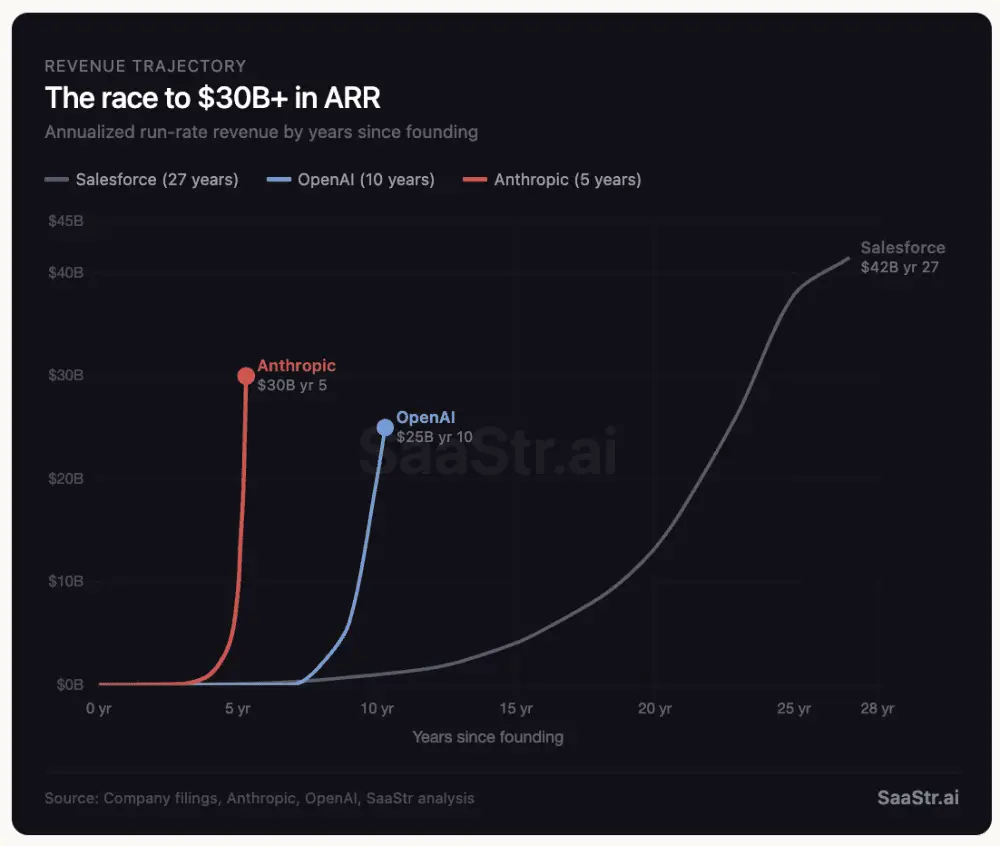

The velocity of AI-native revenue accumulation demands immediate recalibration from every sovereign wealth fund, government-backed venture vehicle, and infrastructure allocator across the Middle East and North Africa. Salesforce required twenty-seven years and a ground-up enterprise sales apparatus to reach $42 billion in annual revenue. Anthropic, incorporated in 2021, touched a $30 billion run-rate within five. OpenAI moved from effectively zero commercial revenue to $25 billion in a decade. These trajectories are not curiosities for Silicon Valley observers; they are capital allocation signals that directly implicate the investment theses of entities such as Mubadala, ADQ, PIF, and the broader constellation of Gulf sovereign capital vehicles that have collectively committed tens of billions of dollars to technology positioning over the past five years.

The structural mechanics driving this compression are consequential for MENA. Consumption-based API pricing eliminates the seat ceilings that historically constrained B2B software penetration in a region where large conglomerates sit alongside high-growth SMEs. Cloud marketplace distribution through hyperscale platforms—AWS, Azure, Google Cloud—means that any Gulf sovereign-backed or venture-supported application company building on frontier models can access the same procurement channels as legacy Western incumbents without replicating two decades of sales infrastructure. For a region actively constructing sovereign AI stacks—Saudi Arabia’s SDAIA, the UAE’s Falcon models, Qatar’s national AI strategy—the implication is stark: the window during which early positioning in the AI application layer generates asymmetric returns is compressing rapidly, and the capital deployed into horizontal AI infrastructure today will define sovereign technological leverage for the next decade.

The profitability caveat, however, cannot be subordinated to headline growth figures. OpenAI is burning roughly $17 billion in cash annually with no projected free cash flow positivity until 2029. Anthropic has absorbed over $67 billion in cumulative funding. Gulf sovereign allocators accustomed to infrastructure investments with defined payback horizons—real estate, utilities, logistics corridors—must internalize that frontier AI bets operate on fundamentally different return curves and carry substantially longer capital lockup periods. The bet these investors are underwriting is that inference costs per unit of intelligence will decline steeply while usage-based revenue compounds, rendering interim losses immaterial against terminal platform value. This is not a traditional infrastructure play with toll-road economics; it is a platform-monopoly bet, and the margin of error between dominance and stranded capital is narrow.

Regional venture and infrastructure strategies must therefore be repositioned around three imperatives. First, application-layer companies built atop Claude, GPT, and open-source models can capture consumption-based scaling without the trillion-dollar compute spend—a thesis directly relevant to MENA fintech, logistics, healthcare, and government-services verticals where local regulatory moats protect against global competition. Second, sovereign capital should prioritize stakes in the cloud distribution and data infrastructure layers—Middle East data center buildouts, regional cloud availability zones, and Arabic-language model fine-tuning capabilities—rather than chasing frontier model training, where the capital requirements are prohibitive and winner-take-all dynamics are already forming. Third, the playbook that Marc Benioff authored over a generation remains valid; the difference is temporal. Salesforce’s twenty-seven-year arc now compresses to under ten. For MENA allocators, the strategic question is no longer whether to engage the AI value chain, but whether deployment speed matches the velocity of the curve itself.