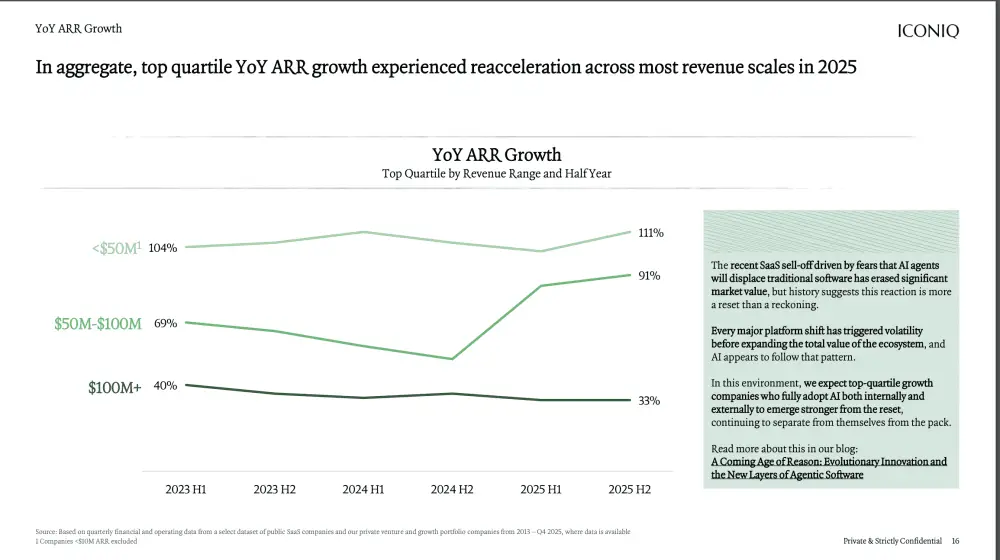

The market has bifurcated dramatically: while the median B2B firm is contracting for the third consecutive year, AI-native startups are achieving exponential growth rates that dwarf traditional SaaS benchmarks. In the $2M‑$10M ARR segment, top‑quartile funded companies are expanding at 515% YoY—a gap of nearly threefold compared to the sector median—while AI‑first entrants are scaling to $100M ARR in 1‑2 years versus the 5‑plus years previously required. This divergence creates a stark strategic choice for incumbent firms across the Middle East and North Africa; those that fail to reposition themselves risk being relegated to the declining cohort, whereas those that capture the asymmetric upside can unlock sovereign capital inflows.

Sovereign wealth entities in the GCC and broader MENA region are accelerating allocations toward high‑growth technology funds precisely because of this bifurcation. Limited partners are demanding exposure to AI‑centric growth vectors that can absorb capital at velocity, and venture capital firms operating locally are structuring dedicated AI‑growth platforms to meet that demand. The implication is clear: sovereign‑driven capital will increasingly target deals that demonstrate Tier‑1 Net Revenue Retention (>110%) and AI‑enhanced product‑market fit, compelling founders to recalibrate pitches around macro‑level capital efficiency metrics rather than traditional unit economics.

Infrastructure implications are equally consequential. Rapid AI adoption mandates robust, low‑latency data ecosystems—from sovereign cloud zones and edge‑compute clusters to fiber‑optic backbone extensions across the Gulf and Maghreb—to sustain the accelerated growth trajectories of startups and multinational entrants. Governments are responding with multi‑billion‑dollar investments in AI‑ready zones, regulatory sandboxes, and up‑skilling initiatives that align talent pipelines with the continent’s emerging tech ambition. Failure to integrate these infrastructural levers into capital deployment strategies will erode the competitiveness of the region’s growth agenda.

In this hyper‑accelerated environment, the decisive lever is speed of execution. Founders must secure high‑conviction funding rounds, embed AI‑driven growth engines, and activate sovereign‑backed partnerships that fast‑track market access. Delaying strategic pivots not only cedes market share to rivals but also forfeits the outsized capital and infrastructure commitments that are reshaping the MENA tech landscape. The opportunity window is narrow; the cost of inaction is systemic decline.