Saudi Arabia’s hydrogen generation market is poised to expand from an estimated $1.63 billion in 2025 to $2.32 billion by 2034, reflecting a modest compound annual growth rate of roughly 4 %. While the headline figures suggest a gradual upward trajectory, the underlying dynamics are being reshaped by the convergence of artificial‑intelligence‑driven optimisation, sovereign‑backed megaprojects, and a deliberate push to position the Kingdom as a global export hub for green hydrogen and its derivatives.

AI applications are already delivering tangible efficiencies across the value chain. Real‑time control algorithms are cutting electrolyzer energy waste by 15‑20 %, machine‑learning forecasts are aligning production with renewable peaks, and predictive‑maintenance platforms are extending asset lifespans while curbing unplanned downtime. These technologies not only improve the economics of green hydrogen but also de‑risk the capital‑intensive infrastructure that Vision 2030 is mobilising, thereby attracting both sovereign funds and international venture capital seeking exposure to scalable decarbonisation assets.

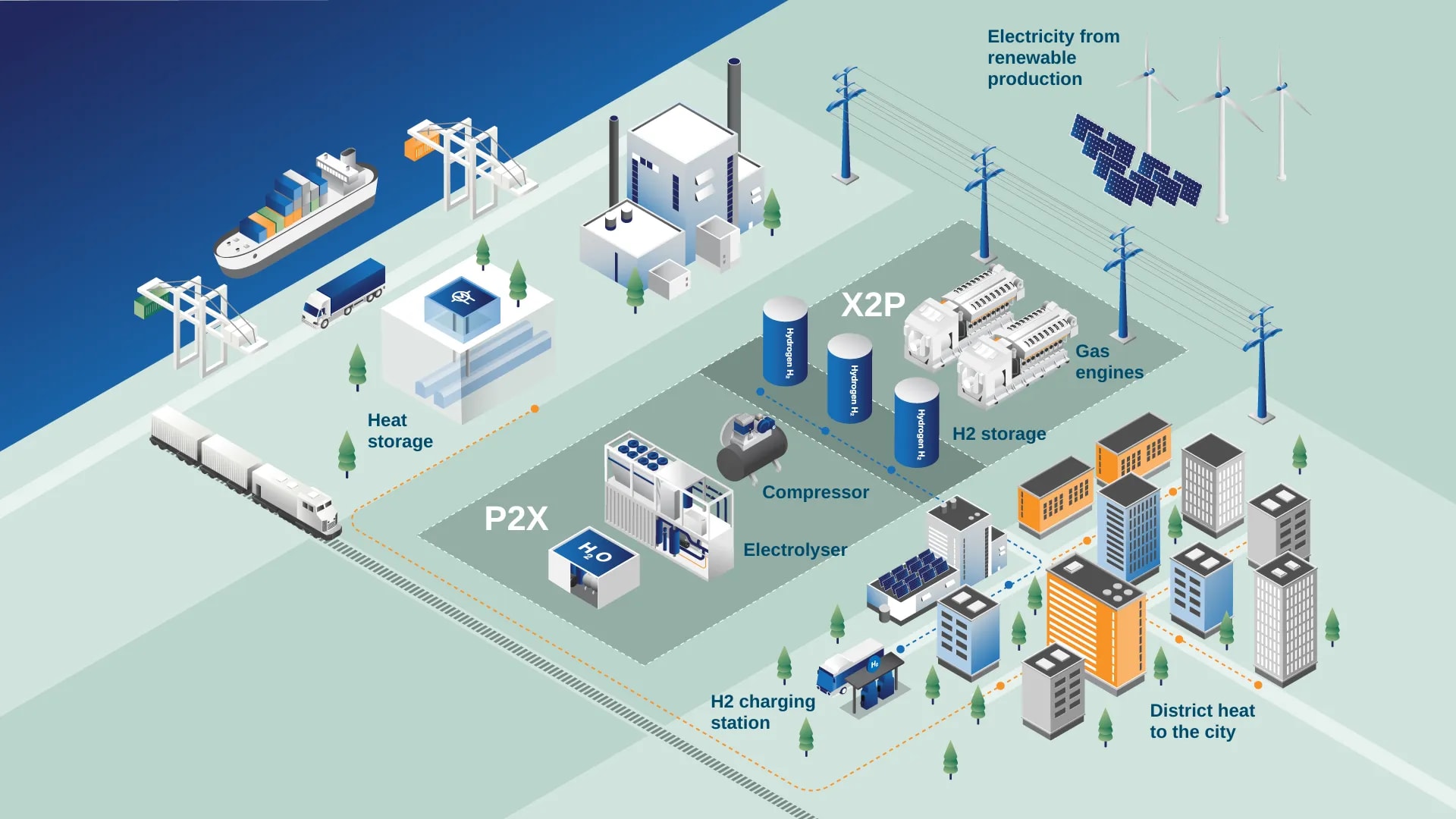

The NEOM Green Hydrogen Project epitomises this strategy: an $8.4 billion joint venture backed by ACWA Power, Air Products and the NEOM authority, now 90 % complete and slated to deliver 600 tonnes of green hydrogen daily from 2027. Financed through $6.1 billion of non‑recourse debt from a syndicate of 23 global banks and supported by offtake contracts with Air Products and SEFE, the project creates a hydrogen‑to‑ammonia bridge to Europe and establishes a template for subsequent hubs such as the planned Yanbu facility. Parallel demonstrations by Saudi Aramco of blue‑ammonia supply chains and fuel‑cell vehicle trials with Toyota and Hyundai further validate the logistics and end‑use markets needed for regional scaling.

From a regional perspective, Saudi Arabia’s hydrogen push is catalysing ancillary infrastructure upgrades—dedicated renewable‑energy parks, desalination‑brine valorisation, and specialised port facilities—across the Northern, Central, Western and Eastern zones. The Kingdom’s ability to lock in long‑term sovereign financing, secure strategic technology partnerships (Thyssenkrupp, Topsoe, Baker Hughes, Hysata), and cultivate a skilled workforce through KAUST‑led research initiatives positions it to become a cornerstone of the MENA low‑carbon economy, offering investors a clear pipeline of bankable projects that combine energy transition credibility with attractive risk‑adjusted returns.