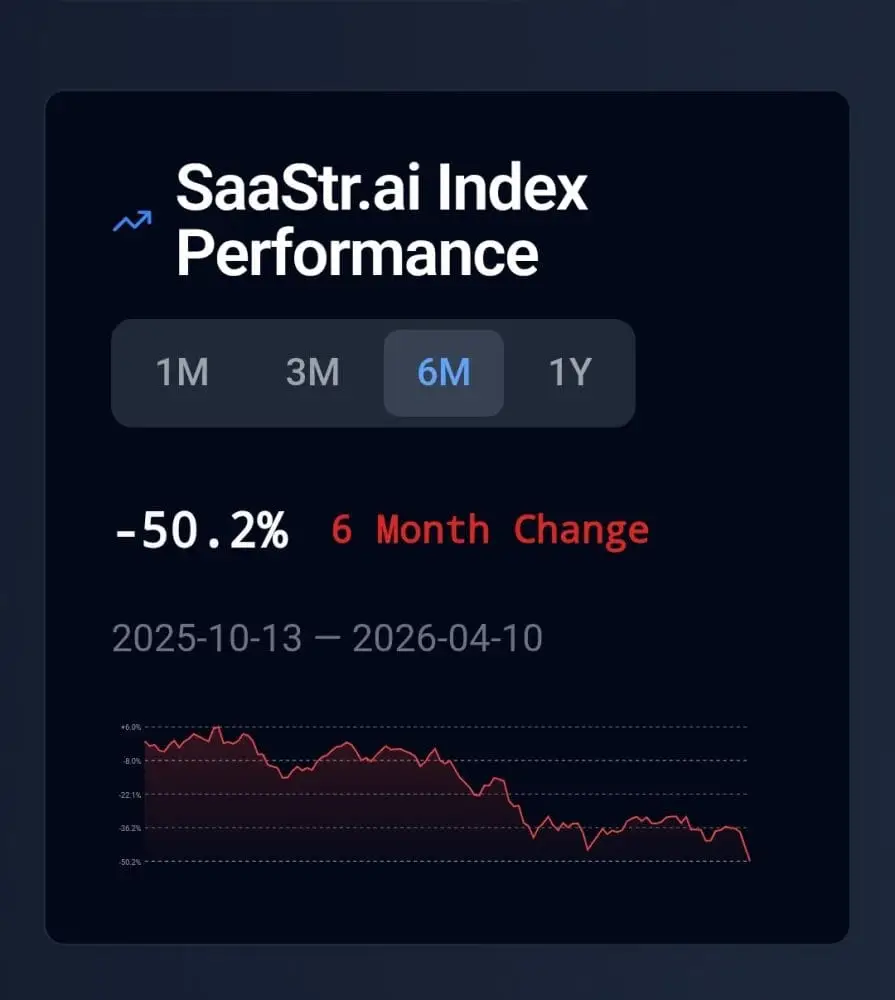

The SaaStr.ai Index – the benchmark that tracks the market value of the 25 most‑quoted public B2B software firms – has slumped 50.5% between October 2025 and April 2026, wiping out roughly half of the sector’s combined market capitalisation. For the first time since the advent of cloud computing, SaaS equities trade at a price‑to‑earnings discount to the S&P 500, with forward multiples collapsing from 84 × in 2021 to just 22.7 × today. This structural re‑rating is being felt across the Gulf and North‑African sovereign wealth funds, which have long allocated a sizable slice of their portfolios to global software champions. The abrupt erosion of valuations forces these funds to reassess exposure, consider reallocating capital toward assets that underpin AI‑driven infrastructure rather than seat‑based productivity suites whose growth prospects are now in doubt.

Two converging forces explain the rout. First, corporate CIOs are re‑budgeting away from traditional SaaS licences toward AI‑centric compute – an estimated $450 billion of hyperscaler spend in 2026 is now earmarked for AI infrastructure, siphoning money that once fed Salesforce, ServiceNow and HubSpot licences. Second, the market is pricing in a substitution risk: generative‑AI agents could supplant the very human‑centric workflows that seat‑based SaaS monetises, compressing terminal‑value assumptions that historically accounted for 85‑95 % of SaaS valuations. The implication for regional venture capital is clear – funds must pivot from backing pure‑play SaaS start‑ups to those that offer low‑level AI‑ready platforms, data‑layer services, or security primitives that become indispensable in AI‑heavy stacks.

Within the wreckage, a clear bifurcation has emerged that mirrors the investment thesis gaining traction in the Middle East. Companies such as Palantir, Cloudflare and DigitalOcean – all providers of AI‑compatible infrastructure – have either maintained growth or outperformed the broader index, whereas traditional workflow vendors like Atlassian, Workday and Adobe have seen their valuations halve. Sovereign investors and regional VC houses are therefore channeling new capital into “AI‑infrastructure” bets – edge computing, high‑throughput networking and secure API‑gateway solutions – that generate demand rather than face substitution. This shift aligns with national digital‑economy strategies that prioritize AI‑enabled cloud services, positioning the MENA region to capture a share of the $40‑50 billion AI spend that is swiftly being re‑routed from legacy software budgets.

For founders of B2B software targeting MENA markets, the message is unequivocal: the era of growth predicated on expanding employee headcount is over. Business models must evolve to capture the AI budget that sovereigns and large enterprises are now authorising, either by embedding AI agents directly into the product stack or by becoming the underlying infrastructure that powers those agents. Private‑round multiples have already contracted from historic 22 × ARR to just 4 ×, eroding the premium that once insulated high‑growth start‑ups from market cycles. Companies that cannot articulate a clear AI‑infrastructure value proposition risk seeing their valuations implode alongside their public‑market peers, while those that position themselves as indispensable components of the AI stack stand to benefit from both regional sovereign inflows and a new wave of venture capital backing.