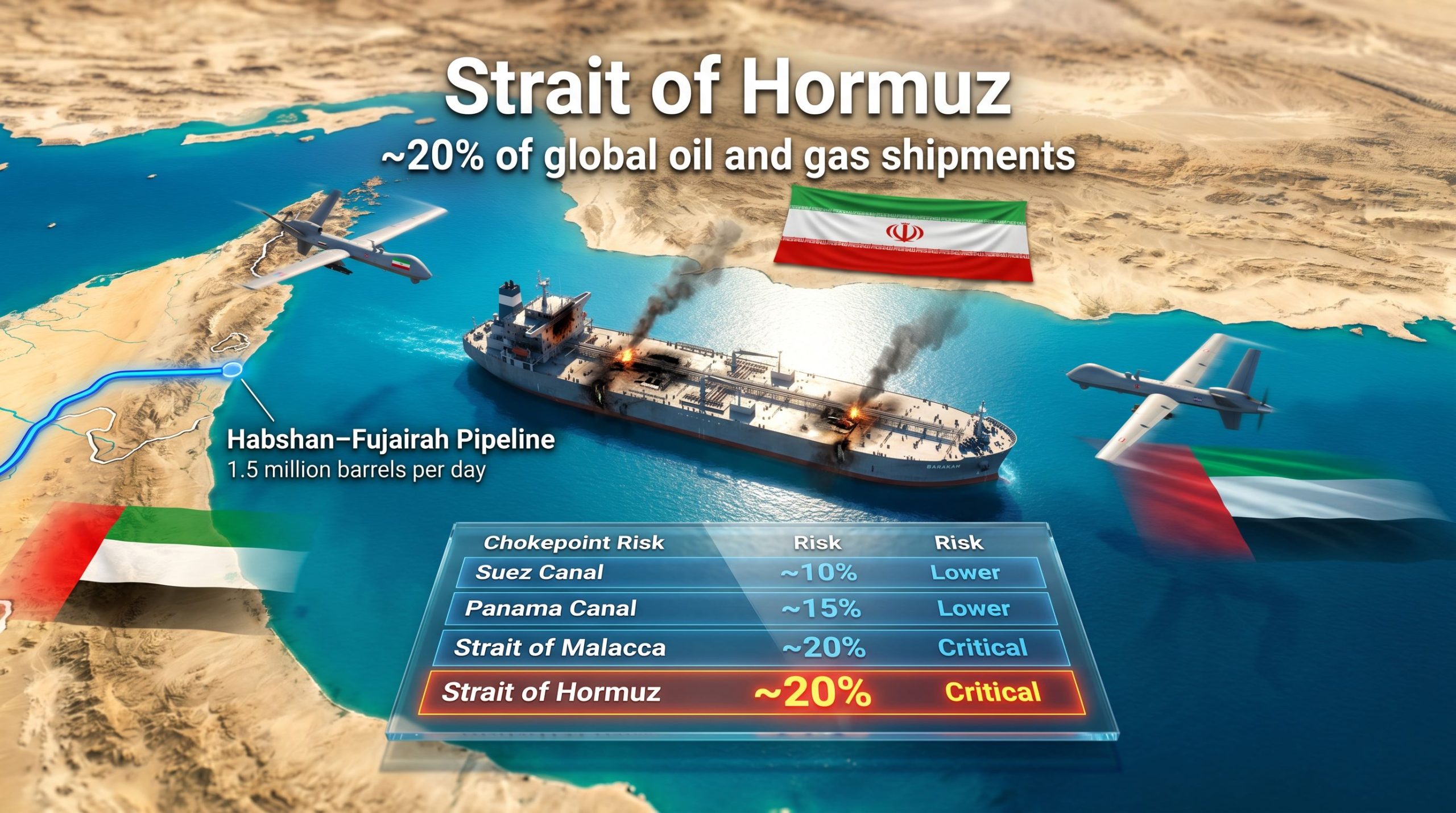

The May 4 attack on the ADNOC‑operated tanker Barakah marks the first overt strike against a sovereign‑owned asset in the Strait of Hormuz since Iran’s February 2026 blockade declaration. By targeting a state‑controlled vessel, Tehran signalled a willingness to jeopardise the legal sanctity of transit passage under UNCLOS, thereby intensifying geopolitical risk for the Gulf’s sovereign wealth funds, which underpin more than $800 billion of regional capital. The incident has already prompted the UAE to invoke multilateral mechanisms—including a formal UN‑Security‑Council referral and coordinated GCC condemnation—raising the prospect of sanctions‑linked insurance spikes that could erode the profit‑margin buffer of national oil companies and curtail the flow of sovereign‑backed venture capital into downstream and renewable projects across the MENA region.

From an infrastructure standpoint, the event underscores the limited redundancy of the Gulf’s export network. While the Habshan‑Fujairah pipeline delivers roughly 1.5 million barrels per day, it covers only a fraction of ADNOC’s total outbound volumes, leaving the majority of crude still dependent on the Hormuz corridor. The absence of an alternative maritime route—given the prohibitive time‑ and cost‑penalties of a Cape‑of‑Good‑Hope detour—means any prolonged interdiction will force regional exporters to re‑route cargoes, inflating freight rates and war‑risk premiums. This structural bottleneck is likely to accelerate capital allocation toward new pipeline projects, offshore loading terminals, and digital tracking systems, sectors where regional sovereign investors and emerging VC funds are already seeking high‑return opportunities.

Market repercussions have rippled through linked asset classes. The credible threat of sustained Hormuz disruption lifted crude‑price volatility indices by over 30 percent within days, while war‑risk premiums for Gulf transits surged to multi‑year highs, compressing shipping margins and prompting a re‑pricing of exposure in energy‑focused hedge funds. Simultaneously, the aviation and real‑estate subsectors—key revenue streams for Gulf sovereign investors—recorded a 60 percent slump in passenger traffic and heightened liquidity strains, respectively, signaling a broader contraction in discretionary spending that could dampen the pipeline of private‑equity and VC deals targeting the region’s diversification agenda.

Looking ahead, three trajectories dominate strategic forecasting: a negotiated de‑escalation that would restore normal transit and stabilize insurance markets; a low‑intensity stalemate that sustains elevated freight costs and preserves a high‑risk premium environment conducive to infrastructure‑centric investment; or a full closure that triggers IEA strategic‑reserve releases and compels an emergency influx of defence‑related capital into the Gulf. For investors and policy‑makers alike, the decisive factor will be how swiftly sovereign capital can be mobilised to reinforce alternative export infrastructure, thereby mitigating Hormuz’s chokepoint‑induced systemic risk and preserving the region’s broader diversification pipeline.