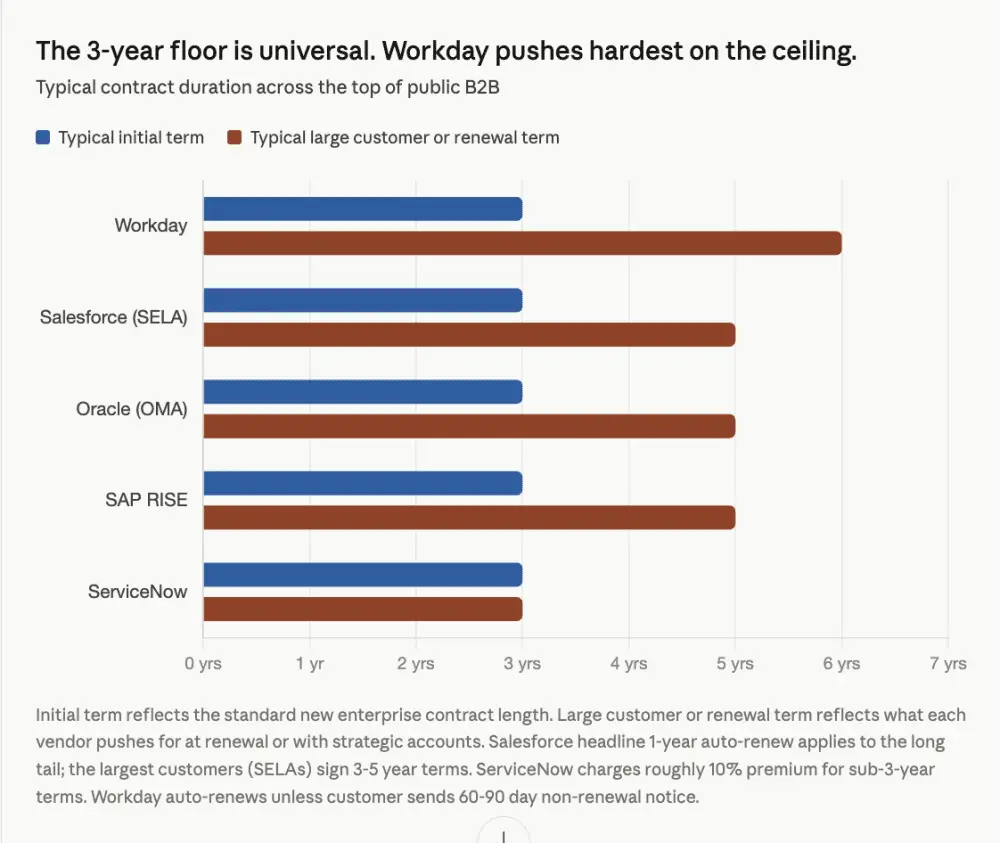

Workday and ServiceNow continue to dominate the global enterprise‑software ledger, posting Gross Revenue Retention (GRR) rates of 97 % and 98 % respectively. In the Middle East and North Africa, where sovereign wealth funds and sovereign‑linked private‑equity vehicles are increasingly allocating capital to cloud‑native platforms, the headline‑grabbing retention metrics mask a structural reliance on multi‑year contracts rather than genuine product stickiness. Both firms default to three‑year initial terms—Workday even pushes five‑ to six‑year renewals—while ServiceNow levies a 10 % premium for shorter, one‑year deals. This contractual scaffolding inflates GRR figures, allowing the companies to report 90 %+ retention even if a substantial slice of renewals is lost each year. For regional investors, the key question is not the nominal GRR but the durability of the underlying business model when contracts inevitably come up for renewal in a market that is rapidly embracing AI‑driven, subscription‑flexible alternatives.

The MENA sovereign investment community is poised to reevaluate exposure to these legacy SaaS giants as AI‑native competitors accelerate product cycles from the typical five‑year disruption horizon to under two years. ServiceNow’s ITSM suite sits squarely in the cross‑hairs of generative‑AI agents capable of automating ticket triage and workflow orchestration, while Workday’s human‑capital management (HCM) and finance modules face emerging AI‑enhanced platforms that can unbundle and replace the most frequently used functions. Unlike SAP or Oracle, whose entrenched ERP ecosystems generate prohibitive migration costs, Workday and ServiceNow are more vulnerable because they lack deep, irreplaceable lock‑in and therefore are more likely to see a rapid shift in new‑logo acquisition—a leading indicator that MENA‑based venture funds are already tracking in the region’s burgeoning AI‑SaaS pipeline.

From an infrastructure standpoint, the shift toward shorter, annual or even monthly contracts will pressure regional data‑center strategies and public‑cloud partnerships. Sovereign cloud initiatives in Saudi Arabia, the UAE and Qatar, which have been built around long‑term commitments with established vendors, must now accommodate a more fluid procurement environment where enterprises demand agility and the ability to switch providers on a yearly basis. This creates opportunities for local cloud operators and system‑integrators to position themselves as neutral platforms that can host multiple AI‑enabled SaaS solutions, thereby mitigating the risk of vendor lock‑in while still capturing a share of the escalating spend on enterprise software.

Consequently, investors and policymakers should shift their analytical focus from headline GRR numbers to four more granular metrics: net new customer growth, the evolving mix of contract durations, Net Revenue Retention (NRR) trends, and renewal‑cycle conversion rates. The early erosion of new‑logo momentum or a pivot toward shorter contracts in the Gulf’s public‑sector procurement documents would signal that the current retention illusion is fraying. Aligning sovereign capital, venture allocations, and regional cloud infrastructure development with these leading indicators will be essential to safeguard long‑term value creation as the AI era redefines the economics of enterprise software across the MENA region.