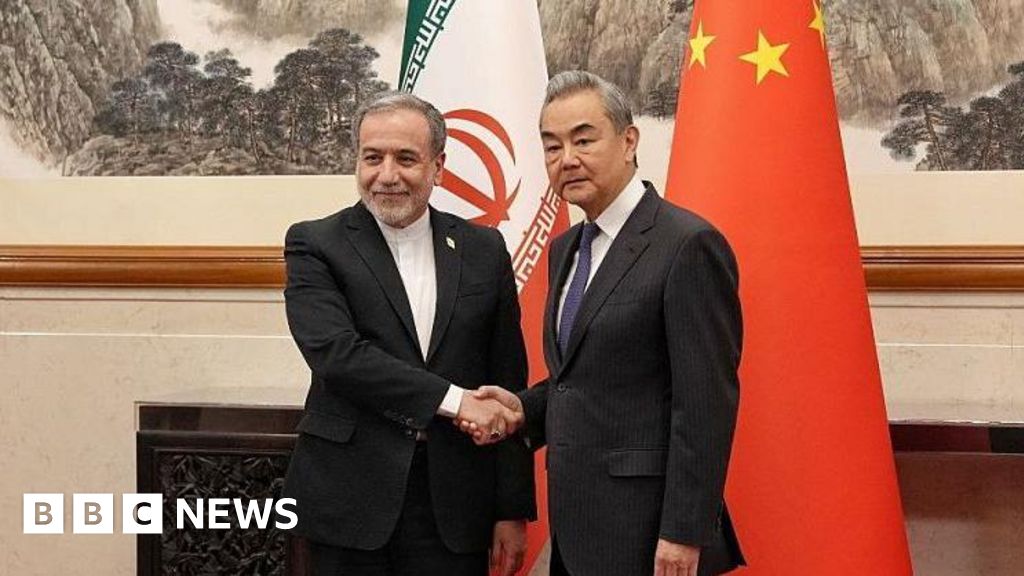

China’s deepening diplomatic engagement with Iran, underscored by Foreign Minister Wang Yi’s talks with Iranian counterpart Abbas Aragchi, signals a pivotal moment for Middle Eastern geopolitics and investment flows. Aragchi’s first post-war visit to Beijing comes amid Tehran’s efforts to circumvent Western sanctions and recalibrate its economic partnerships, with the Belt and Road Initiative (BRI) serving as a cornerstone for renewed collaboration. For the MENA region, this thaw points to an accelerated shift toward multipolar trade corridors, where sovereign capital from Gulf states and Chinese state-backed enterprises converges to fund energy, logistics, and digital infrastructure projects. The UAE and Saudi Arabia, already key BRI partners, are likely to leverage this dynamic to diversify their own geopolitical and economic risks, particularly as they navigate post-oil transitions and regional security recalibrations.

The implications for regional venture capital are stark. Iran’s vast untapped markets, coupled with China’s tech and manufacturing prowess, could catalyze cross-border investments in sectors like renewable energy, fintech, and telecommunications. Sovereign wealth funds from the Gulf, including Mubadala and Saudi Arabia’s PIF, may find renewed opportunities to co-invest in Iran’s unpenetrated frontier markets, particularly if sanctions ease. However, regulatory uncertainties and security concerns will test the appetite of institutional investors, requiring robust risk mitigation frameworks. Meanwhile, China’s financing of critical infrastructure—ports, railways, and 5G networks—could reshape trade routes, reducing dependency on traditional Western-dominated supply chains and bolstering MENA’s role as a bridge between Asia, Africa, and Europe.

This realignment also threatens to strain Western influence in the region, as Gulf capitals hedge against U.S. pressure by deepening ties with Beijing. The U.S. risks ceding economic leverage to China, particularly if Iranian crude sales to Asia ramp up, further entrenching Tehran’s position as a linchpin in Eurasian energy markets. For regional infrastructure, the surge in Chinese capital could fast-track megaprojects like the China-Pakistan Economic Corridor’s western extensions, indirectly benefiting MENA’s logistics landscape. Yet, overdependence on Chinese funding poses risks, as seen in debt distress cases across Africa and Southeast Asia, forcing MENA policymakers to balance opportunity with fiscal prudence.

As the war in Gaza and broader Middle Eastern instability persist, China’s Iran outreach reflects a calculated play to position itself as the region’s primary alternative power broker. This shift reverberates through global commodity markets, with Brent crude futures likely to benefit from increased Iranian export capacity, while regional currencies face pressures from heightened geopolitical volatility. For investors, the key takeaway is clear: MENA’s economic architecture is entering a phase of rapid realignment, driven by sovereign pragmatism and strategic capital flows that prioritize long-term influence over short-term gains.