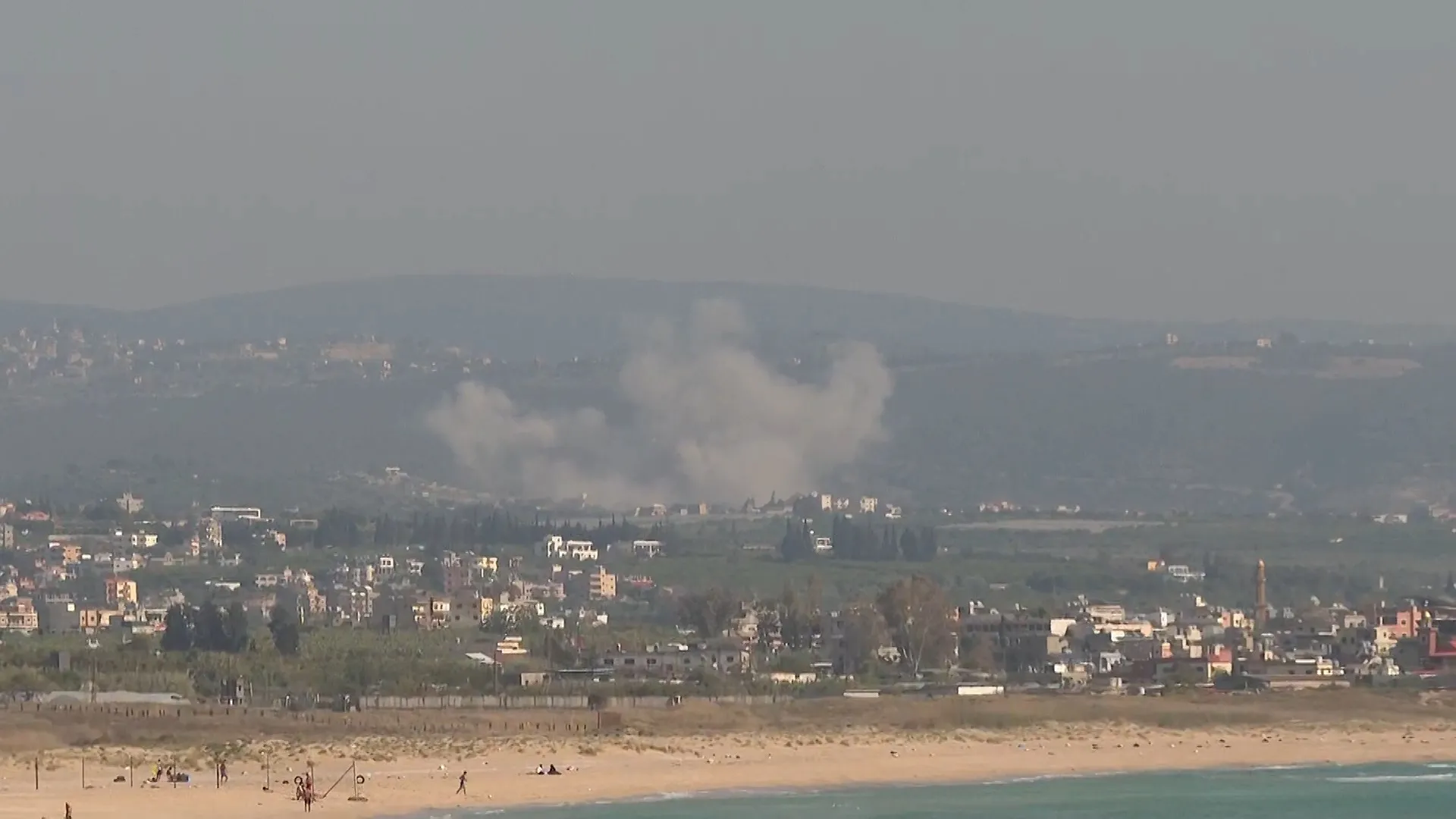

The recent surge in Israeli airstrikes across southern Lebanon has sharply heightened geopolitical volatility in the Levant, prompting a rapid reassessment of risk parameters among regional investors. The incident underscores the fragility of cross‑border security frameworks and is likely to elevate country‑level risk spreads for Lebanon‑adjacent markets, especially those with fiscal exposure to external shocks.

Middle‑Eastern sovereign wealth funds, notably the Gulf Cooperation Council’s publicly listed vehicles, are expected to tighten reins on risk‑laden assets and increase allocations to low‑beta instruments such as U.S. Treasury proxies or diversified infrastructure holdings. These funds may also redirect a portion of their capital toward resilience‑focused projects, seeking to hedge against geopolitical fallout while preserving long‑term yield targets.

Venture and private‑equity markets are positioning to capture emerging demand for defense‑adjacent technologies, cybersecurity solutions, and logistics platforms that enhance supply‑chain resilience for critical imports into the Gulf. Start‑ups specializing in satellite communications, autonomous security systems, and disaster‑response analytics are receiving heightened scouting interest, given the heightened demand for scalable, defensible tech in an unstable security environment.

Infrastructure planning across the broader MENA region is poised for a recalibration toward redundancy and multi‑modal redundancy. Projects slated for cross‑border freight corridors, renewable‑energy grid interconnectivity, and hardened energy transmission networks are likely to attract increased sovereign and private financing, as governments prioritize security‑compatible assets that can withstand intermittent conflict spikes and ensure uninterrupted economic flows.