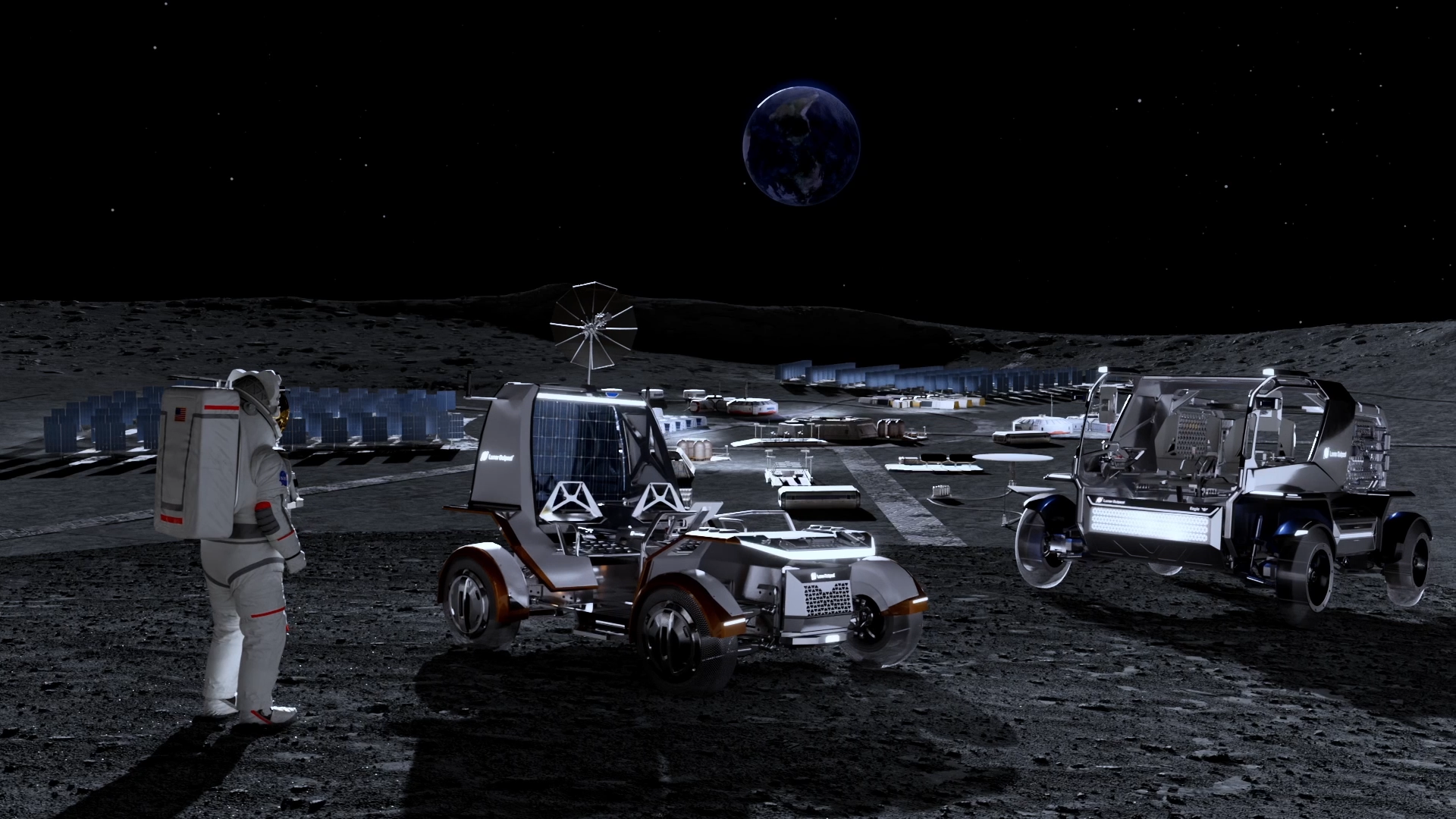

LunarOutpost’s $30M Series B fundraising underscores a strategic pivot in global space exploration investment, with implications reverberating across sovereign capital strategies and venture capital ecosystems in the MENA region. The round, led by Industrious Ventures with participation from specialized funds, reflects a growing recognition of the sector’s potential to catalyze technological leadership and economic diversification. For MENA nations pursuing sovereign capital strategies aligned with high-growth frontier technologies, this trend signals a critical inflection point. As the U.S. commits $20B to establish a lunar base by 2030, regional entities may seek to position themselves as suppliers or partners in this burgeoning ecosystem. The demand for lunar mobility solutions, exemplified by Lunar Outpost’s Pegasus rover—a streamlined, cost-effective alternative to prior models—demands localized infrastructure development, including advanced manufacturing hubs and R&D centers. MENA’s geographic and economic profile positions it to capitalize on this shift, particularly through state-backed initiatives targeting sovereign capital outflows into global supply chains.

At the business level, the lunar tech boom presents MENA with transformative opportunities to modernize regional infrastructure and attract sovereign and VC capital. The necessity for scalable, lightweight rovers and surface tech aligns with pilot programs in countries like UAE and Saudi Arabia, which are aggressively investing in aerospace and defense sectors as part of diversified growth agendas. However, this requires substantial upfront investment in specialized industrial capacity, which may strain regional financial resources in the short term. Sovereign entities in the region could explore co-investment models, leveraging lunar exploration contracts to offset costs while advancing national technology ambitions. Meanwhile, venture capital firms based in MENA, recognizing the sector’s macroeconomic potential, may begin to siphon resources toward space-adjacent startups, mirroring global patterns observed in Silicon Valley. This shift would necessitate enhanced regulatory frameworks to foster innovation while mitigating risks associated with unproven technologies, a challenge MENA governments must navigate proactively.

Ultimately, the success of Lunar Outpost’s expansion hinges on its ability to secure NASA’s Lunar Terrain Vehicle Services contract—a decision pivotal to its near-term growth and regional scalability. For MENA, this represents a broader strategic question: how can regional entities attract and compete for global contracts in space technology? The timeline for Pegasus deployment by 2027 coincides with MENA’s anticipated advancements in space infrastructure, potentially allowing countries to offer complementary services such as satellite data analytics or ground station networks. Sovereign investments in lunar tech could also catalyze cross-border collaborations, positioning MENA as a non-Western hub for space innovation. However, this requires aligning regional financial strategies with global geopolitical shifts, particularly as emerging economies vie for influence in next-generation space initiatives. The fundamental challenge remains balancing sovereign capital outflows with localized economic returns, a dynamic that will define MENA’s trajectory in the coming decade.