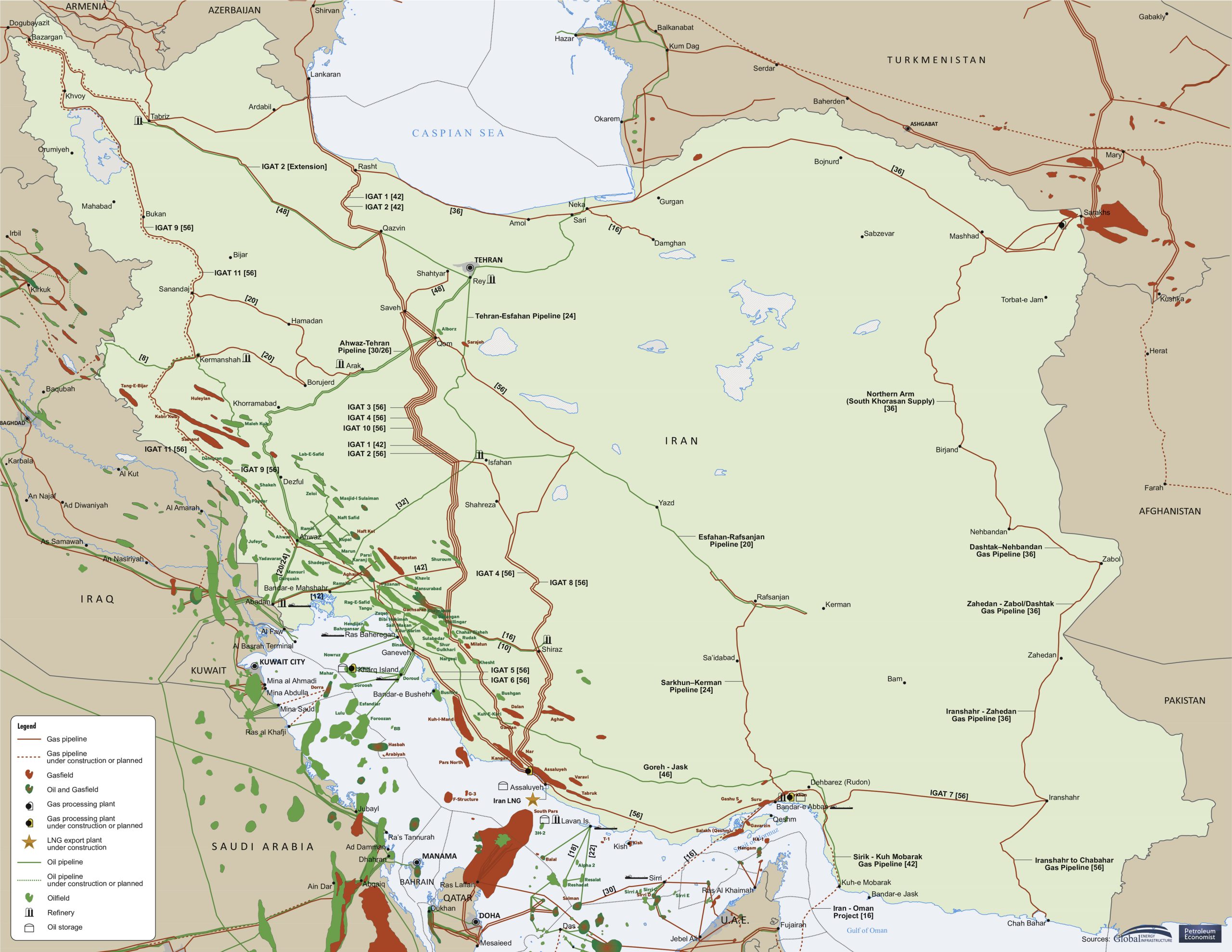

The recent missile attacks on critical energy infrastructure in Qatar and the UAE represent a material disruption to global gas supply chains, with immediate implications for sovereign wealth fund portfolios and regional investment appetites. QatarEnergy’s Ras Laffan complex—the world’s second-largest LNG export hub—sustained extensive damage to its Pearl gas-to-liquids facility and multiple LNG trains, directly threatening the operational integrity of assets co-owned with major international oil companies like Shell. Concurrently, the interception-driven shutdown of ADNOC’s Habshan gas processing complex, which handles 6.1 billion cubic feet per day, underscores the vulnerability of sovereign-owned energy nodes. These events trigger an urgent recalibration of sovereign risk, potentially increasing the cost of capital for Gulf Cooperation Council (GCC) states and pressuring the credit ratings of entities whose balance sheets are anchored in physical asset durability.

Thebusiness fallout will extend beyond immediate repair costs to induce a strategic pivot in capital allocation by the region’s largest sovereign wealth vehicles. With state-owned energy champions like QatarEnergy and ADNOC facing unplanned capital expenditure for reconstruction and enhanced security, discretionary investment in venture capital and non-energy sectors is likely to be constrained. This environment will favor defense, cybersecurity, and critical infrastructure technology startups, while potentially starving broader MENA tech ecosystems of the growth-stage capital historically sourced from entities like the Qatar Investment Authority and Abu Dhabi Investment Authority. The attacks demonstrate that geopolitical stability is a non-negotiable prerequisite for large-scale private capital deployment, making regional VC firms and portfolio companies more susceptible to risk-off sentiment from global limited partners.

Long-term, these incidents will accelerate a mandatory redesign of regional energy infrastructure, blending physical hardening with advanced digital monitoring. Expect sovereign oil and gas majors to fast-track investments in AI-driven perimeter security, drone detection systems, and redundant processing capabilities—a shift that will create a nascent market for specialized industrial cybersecurity and resilience engineering firms within the MENA tech landscape. Furthermore, the attacks underscore the business case for deeper integration of regional air and missile defense networks, moving such cooperation from a purely military domain to a shared economic imperative. The resilience of the GCC’s energy backbone is now a central component of its economic diversification narrative; failure to address this will jeopardize the very infrastructure projects, from hydrogen hubs to industrial zones, that underpin sovereign visions like Saudi Vision 2030 and the UAE’s Operation 300Bn.