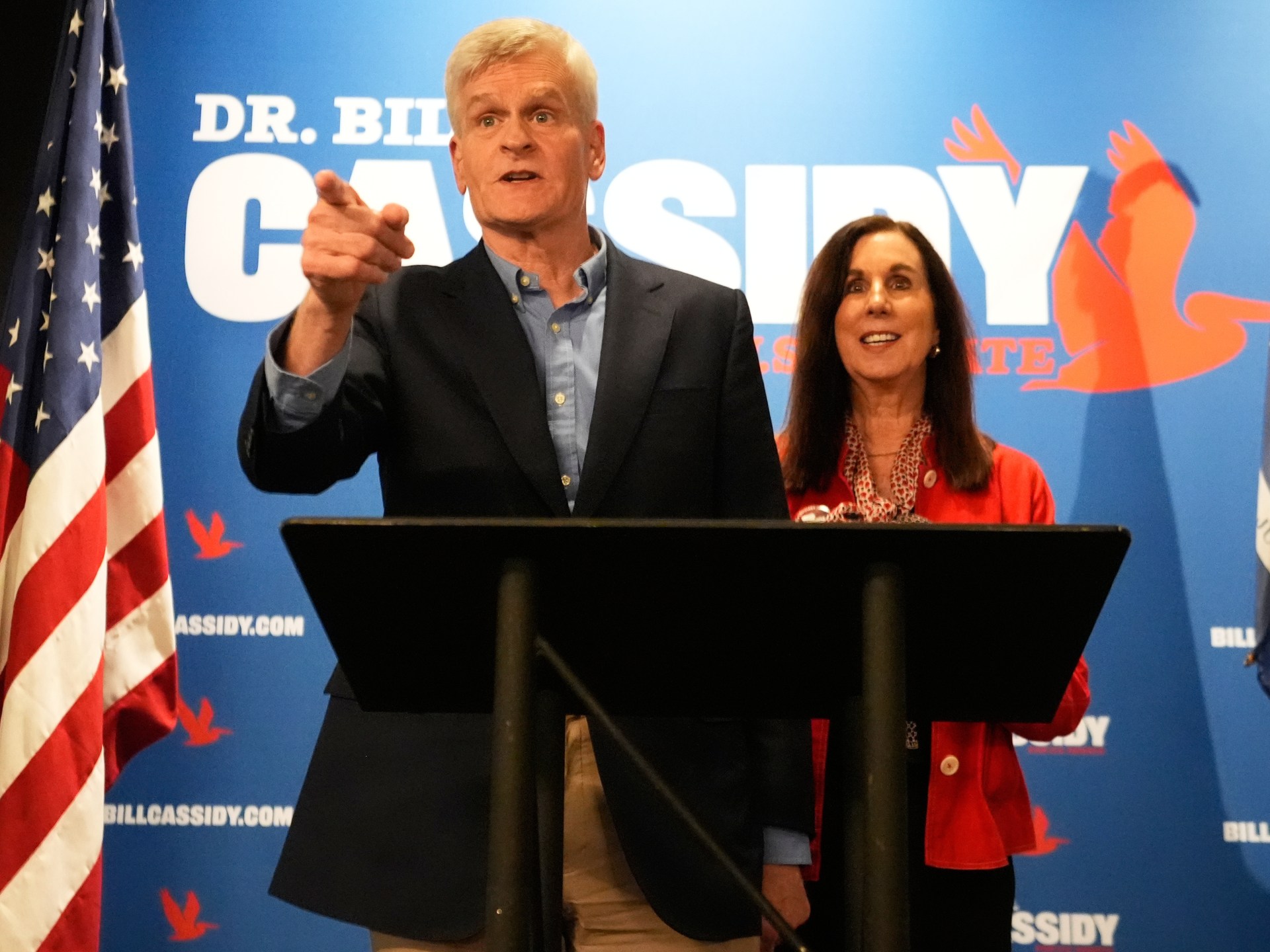

The unfolding Republican primary challenge against Louisiana Senator Bill Cassidy represents a significant case study in the political risk calculus now confronting long-term capital allocators, with direct implications for sovereign wealth funds and venture capital deployment across the MENA region. Cassidy’s 2021 impeachment vote, a rare act of intra-party dissent, has become a focal point for a Trump-loyalist insurgency, signaling a hardening ideological litmus test within the GOP. For MENA investors and sovereigns, this dynamic underscores a persistent source of policy unpredictability in Washington, complicating strategic planning for US partnerships, particularly in energy transition, technology transfer, and defense sectors where bipartisan continuity was once assumed. The potential ouster of a pragmatic, deal-making physician-senator in favor of a more doctrinaire candidate could presage a more transactional and erratic US foreign policy posture, forcing regional capitals to recalibrate their economic and security hedging strategies.

The broader purge of GOP impeachment jurors, leaving only outliers like Collins and Murkowski, illustrates the former president’s enduring capacity to enforce party discipline—a factor that cannot be discounted by fund managers assessing the stability of US regulatory and trade frameworks. This internal consolidation of power occurs even as Trump’s national approval wanes, creating a volatile political environment where traditional governing norms are subordinate to base mobilization. For MENA venture capital, which has increasingly looked to US strategic partnerships and exit markets, such volatility introduces a premium on geopolitical risk assessment. Capital deployment into US-tech joint ventures or infrastructure projects may now require higher contingencies for sudden policy reversals, particularly concerning sanctions, technology export controls, and energy investments, as the party’s center of gravity shifts further toward economic nationalism and away from established multilateral channels.

Furthermore, the primary occurs against the backdrop of a Supreme Court-sanctioned redistricting battle in Louisiana, a process that will likely dilute Black-majority representation. This domestic struggle over voting rights and demographic power directly correlates with the policy priorities that MENA sovereigns monitor when engaging with US political leaders. A congressional map engineered to maximize Republican advantage could entrench a more homogeneous and hard-line legislative caucus, less inclined toward the nuanced diplomacy required for complex MENA statecraft. Infrastructure deals, from port leases to 5G network partnerships, often require delicate bipartisan support; a legislature more polarized along Trumpist lines may prove a less reliable counterparty. Consequently, regional sovereign wealth funds and state-linked enterprises may accelerate efforts to diversify their international partnerships, channeling more capital toward Asia, Europe, or intra-regional projects to mitigate exposure to US political cycles.

Ultimately, the Louisiana primary is a microcosm of a wider trend: the subordination of institutional governance to personalist politics. For the MENA region, where many states are pursuing ambitious, capital-intensive visions—from Neom to logistic mega-hubs—the reliability of the United States as a stable, long-term partner is under renewed scrutiny. The capital flight risk is not immediate, but the premium on political risk insurance, the structuring of off-balance-sheet entities, and the search for alternative anchor investors is rising. As Trumpism solidifies its grip, the era of assuming a predictable, pro-business Republican party is over, compelling a fundamental reassessment of how MENA capital engages with the American political economy. The cost of this uncertainty will be measured in delayed projects, higher financing costs, and a strategic pivot toward geopolitical blocs less susceptible to domestic political convulsions.