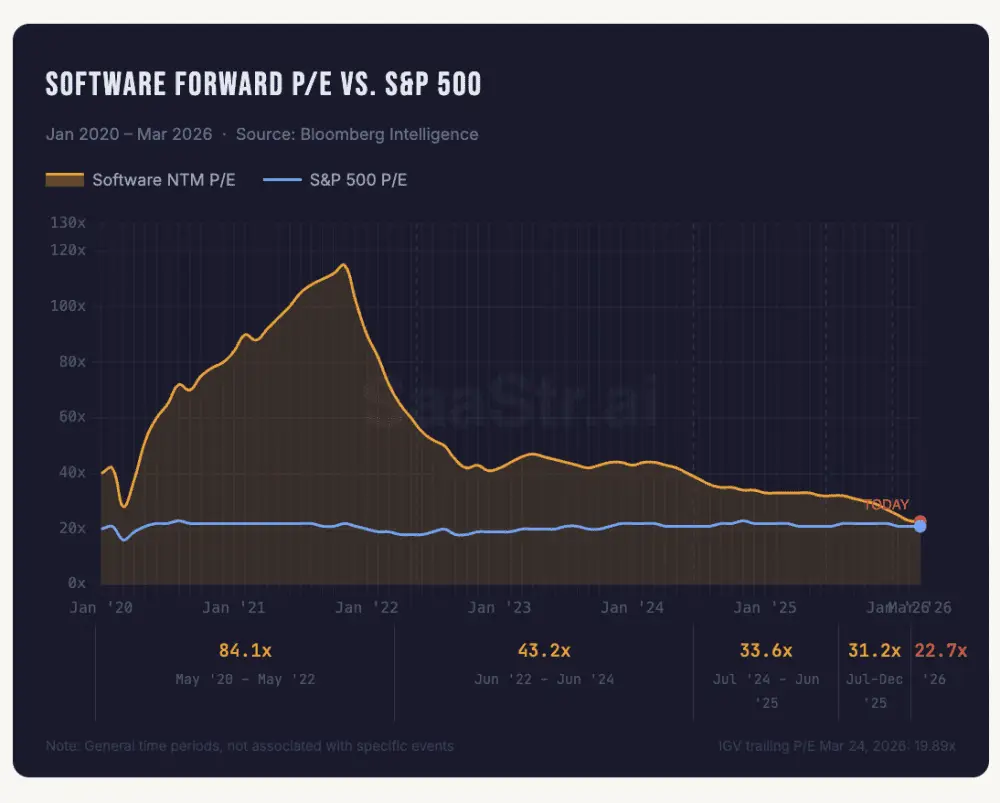

Software valuations in the U.S. have fallen below the S&P 500 multiple for the first time on record, a seismic shift in asset pricing that signals more than a cyclical unwind. At 22.7x forward earnings in Q1 2026—versus average tech premiums of 2-4x over the past decade—public software companies have shed $2 trillion in equity value since last year. IGV, the primary software ETF, has now declined more than 30% from its September 2025 peak. While previous tech corrections reflected valuation excesses or macroeconomic stress, this mark-down is driven by concerns over structural disruption—particularly the displacement of seat-based revenue models by AI-driven automation.

For Middle East and North African institutional investors, this marks a moment of tactical reassessment. Regional sovereign wealth funds, already committed to technology uplift through initiatives like Saudi Vision 2030, must balance exposure between legacy SaaS equities and ascendant AI-native platforms. The same caution applies to regional private equity sponsors, whose portfolio assumptions around enterprise software exits are being re-rated in real time. With global seat compression threatening conventional growth engines, MENA VCs will need to refine diligence methodologies to better interrogate AI defensibility and alternative top-line drivers—particularly for startups targeting productivity or enterprise workflow incumbents.

Infrastructure impact is pronounced. Cloud and data center demand, shaped by AI workloads, will surge, but with capital expenditure increasingly allocated to hyperscale players—often subsidizing performance of legacy tools they now eclipse. This shifts the balance in multi-cloud strategy: MENA tenants are now requiring deeper AI integration in hosted environments to avoid redundancy. Moreover, regional fund managers are scaling back late-stage SaaS allocation in favor of earlier-stage AI and developer-infrastructure bets, recalibrating carry-home expectations. Sovereign capital, especially from resource-based balance sheets, is likely to retain selective exposure to software, but only where AI-native models or vertical integration can credibly offset the disruptive signals emanating from public markets.