In the evolving financial and technology landscape of the Middle East and North Africa, the dynamics surrounding B2B software procurement have reached a critical inflection point. The recent shift toward shorter contract cycles—with sub-1-year terms dominating the growth landscape—reflects a fundamental recalibration of risk appetite and strategic agility among sovereign and private sector buyers. This transformation is not merely tactical but represents a structural overhaul in how investment, value capture, and digital transformation are conceptualized across the region’s most promising sectors.

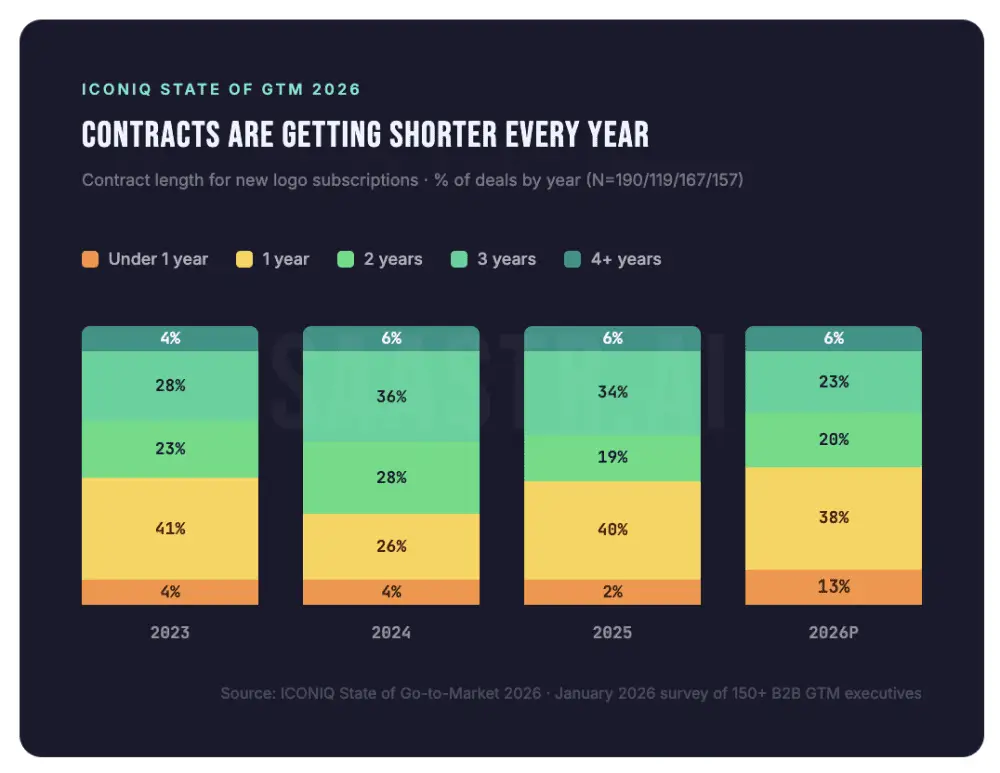

The latest insights from the ICONIQ State of Go-to-Market 2026 underscore the urgency for organizations to adapt rapidly. Substantially more C-suite and procurement leaders are demanding shorter contractual engagements, not due to diminished confidence in AI solutions per se, but because the procurement function is increasingly attuned to the imperative of flexibility in a volatile market. The data highlights a remarkable decline in multi-year contract prevalence, illustrating that buyers are prioritizing immediate utility and scalability over long-term exclusivity. This is reflected in the significant drop in three-year agreements and the acceleration of the transition to shorter timeframes, aligning with compressed decision cycles and heightened market volatility.

Behind this shift lies an underlying recalibration of investor sentiment and the operational imperatives of both corporates and venture capital. Investors seeking stable returns in saturated and rapidly innovating sectors are turning to startups and tech-enabled platforms that can pivot with the speed of execution demanded by emerging needs. For the private equity world, this signals a profound change in capital allocation patterns, favoring nimble players equipped to manage ambiguity and reposition within short cycles. Organizations that fail to recalibrate their go-to-market strategies may find themselves trapped in obsolete commitments or risked disavowed bids in an unforgiving competitive field.

The implications extend beyond operational adjustments to strategic resilience. As the AI-driven software market matures, regional entities must double down on transparency, agility, and relationship-based engagement to remain competitive. Sovereign-backed investors and technology leaders alike must recognize that the new norm is one of continuous renewal and selective commitment—where speed, relevance, and value delivery dictate the terms of any stake. Only those who embrace this paradigm will secure their foothold and deliver enduring value in the intensifying regional battle for digital leadership.