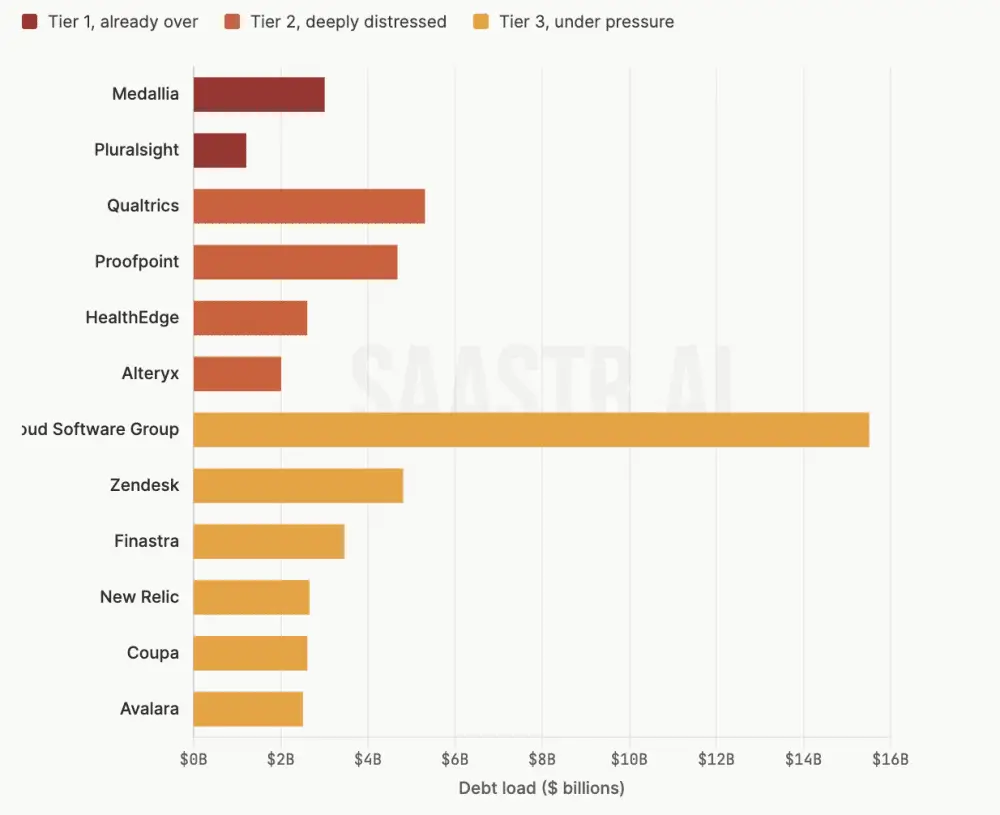

The involuntary transfer of Medallia from Thoma Bravo to its banking syndicate marks the crystallization of a leveraged-financing rupture that extends far beyond a single enterprise software franchise. A $6.4 billion buyout, financed at peak SaaS multiples, has succumbed to the arithmetic of maturity transformation gone wrong: earnings before interest, tax, depreciation and amortisation of roughly $200 million proved insufficient to service $300 million of annual debt service once payment-in-kind forbearance lapsed. The consequence is an equity wipeout and a balance-sheet transfer that hands effective control to Blackstone, KKR, Apollo and Antares. For sovereign wealth funds and state-backed investment vehicles across the Gulf, the Medallia template is a stress test of the private-credit channels that have funded Western technology roll-ups and, increasingly, cross-border deployments into MENA digital infrastructure.

The structural exposure runs deeper than one balance sheet. A $46.9 billion distressed pile of US software debt, with $17.7 billion cascading into stressed territory in a single four-week window, signals that leverage cycles built on 9x revenue multiples and zero-rate carry trades are deflating to 6x realities. This directly constrains the exit horizons for limited partners, including Gulf capital deploying through funds-of-funds and co-investment vehicles. More critically, it recalibrates the cost of capital for platform acquisitions that underpin regional data-center build-outs, cloud migrations and enterprise digitalisation. As refinancing deadlines concentrate ahead of 2028, secondary-market pricing and covenant breaches in names such as Proofpoint, Qualtrics and the broader Vista/Bain/Clearlake cohort suggest that leverage is no longer recyclable. For MENA infrastructure and venture portfolios, this translates into tighter sponsorship dry powder, compressed secondary multiples and an expectation that cash-flow discipline will replace growth-at-any-cost expansion.

Implications for regional venture and sovereign deployment strategies are therefore operational, not hypothetical. Private credit’s entanglement with software means that liquidity constraints in Silicon Valley balance sheets can quickly transmit to funding terms for Middle Eastern tech platforms, logistics networks and fintech ecosystems seeking leverage-backed growth. The contraction of PE as an exit destination shifts the onus onto corporates and infrastructure investors to absorb assets at markedly lower multiples, while venture debt providers are poised to tighten covenant packages. In an environment where seat-based SaaS models face compression from AI-native substitutes, Gulf capital must prioritise infrastructure that monetises throughput and data integrity rather than user-license stacks. The Medallia restructuring is not isolated; it is the leading indicator of a capital-structure reset that will reward balance-sheet resilience and penalise leveraged vintage assumptions from here forward.