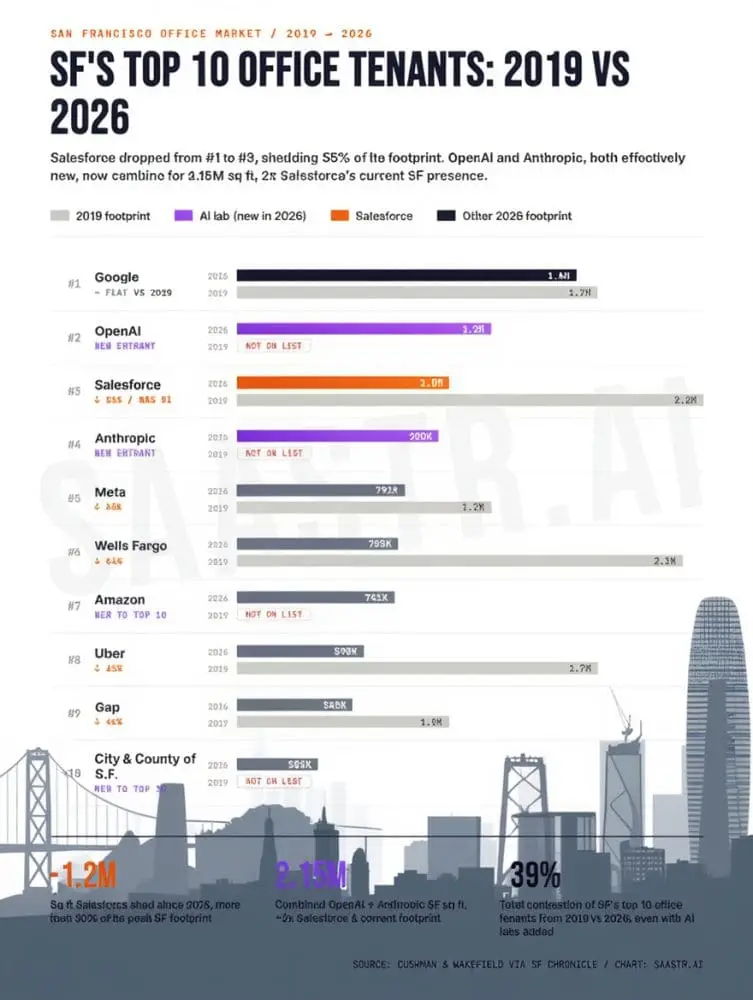

The recalibration of San Francisco’s commercial real estate ledger—where legacy platform champions have surrendered over 5.5 million square feet while artificial intelligence operators have absorbed nearly 2.2 million—serves as an early signal of a broader post-industrial capital reallocation extending into the Middle East and North Africa. For sovereign wealth funds and state-linked investment authorities from Abu Dhabi to Riyadh, the compression of legacy enterprise footprints and the simultaneous vertical integration by AI-native entities underscore a shift from diffuse, multi-tenant commercial strategies to concentrated, capital-intensive infrastructure ownership. In the MENA context, this implies accelerated deployment of sovereign capital toward AI-ready data estates, compute supply chains, and specialized campuses designed to anchor long-term talent and capital lock-up, rather than chasing flexible leasing models that have proven vulnerable to rapid de-risking.

Venture capital allocations across the region will increasingly price the durability advantage embedded in physical infrastructure. The arithmetic of San Francisco shows that AI entrants have replicated the spatial scale of a generational B2B incumbent in under half a decade, a pattern that translates directly into MENA tech hubs where limited near-term liquidity heightens the value of hard assets. Gulf capital is positioned to underwrite hyperscale compute nodes, sovereign cloud backbones, and applied AI laboratories as structural, decade-long bets, effectively substituting the region’s previous preference for platform-enabled real estate arbitrage with asset-backed technology platforms. For limited partners and co-investment consortia, the lesson is explicit: capital directed toward scalable, place-bound AI infrastructure will command optionality as scarce engineering talent consolidates around environments that guarantee long-term resource commitment, while legacy SaaS and consumer-tech footprints face secular right-sizing.

Infrastructure strategy across MENA will pivot to harden nodes that can absorb similar agglomeration effects without importing the West’s cyclical commercial overhang. Sovereign balance sheets and infrastructure funds will prioritize secure power, fiber redundancy, and localized training clusters that transform capital into proprietary spatial advantage, ensuring control over data residency, compute access, and talent retention amid global supply volatility. The implied contract—ten-year physical commitments in exchange for durable clustering efficiencies—will redefine how Riyadh, Dubai, Abu Dhabi, and Cairo channel petro- and non-petro capital into next-generation economic capacity. In doing so, the region will sidestep the legacy enterprise contraction now visible in mature markets and instead deploy sovereign balance-sheet depth to build defensible, AI-centered economic corridors that outlast cyclical headwinds in global venture markets.