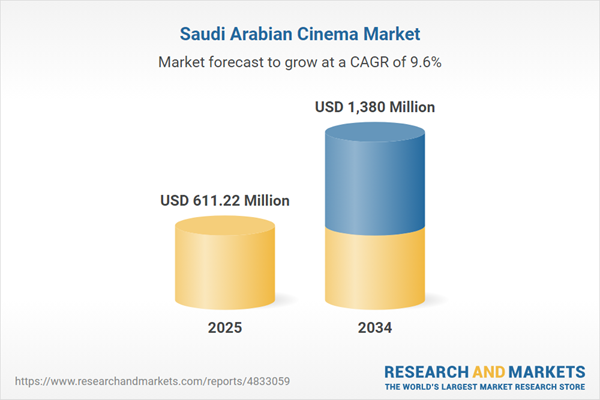

Saudi Arabia’s cinema market, valued at an estimated $611 million in 2025 and projected to exceed $1.3 billion by 2034 at a 9.5% compound annual growth rate, represents far more than a consumer entertainment story. It is a direct manifestation of the Kingdom’s Vision 2030 strategy to channel sovereign capital into sectors that diversify revenue streams away from hydrocarbons. The lifting of the decades-long ban on public cinemas in 2018 unlocked one of the most significant greenfield opportunities in MENA’s entertainment landscape, and Riyadh’s deliberate deployment of public-private partnerships has positioned the Kingdom as the region’s fastest-growing market for multiplex development. Operators such as Muvi Cinemas, AMC, IMAX, Cinepolis, and VOX Cinemas are scaling aggressively, with the government targeting 50 to 100 cinemas by 2030—a buildout trajectory that will require sustained capital expenditure across digital projection, IMAX, 4DX, and luxury seating formats, and that carries meaningful implications for regional commercial real estate and mixed-use development pipelines.

The structural demographic underpinning is unambiguous: over 70% of the Saudi population is under 35, urban disposable incomes are rising, and mobile internet penetration has reached 99% with speeds exceeding 215 Mbps—placing the Kingdom among the top ten globally. These conditions create a uniquely addressable consumption base that venture capital and private equity houses have begun to target with greater precision, not only in exhibition but across the content production and distribution value chain. The emergence of homegrown brands like Muvi, now operating its twenty-second location in Jeddah, signals indigenous entrepreneurial momentum that blends well with both sovereign wealth allocation strategies and external fund interest in scalable Gulf-based entertainment platforms.

From an infrastructure standpoint, the embedding of cinemas within shopping malls and mixed-use developments in Riyadh, Jeddah, Dammam, and the broader Aramco corridor is reshaping footfall economics and anchoring new lifestyle districts. This pattern of entertainment-led urban planning carries broader implications for MENA: it provides a replicable model for economies in the GCC and North Africa that are similarly seeking to monetize young, digitally connected populations through place-based experiential consumption. However, capital intensity remains non-trivial—prime-location lease obligations, technology upgrade cycles, and the energy demands of large-format projection systems compress margins in low-footfall periods, demanding disciplined operatorship and patient capital.

The most consequential strategic tension lies in the competitive dynamics between physical exhibition and digital streaming platforms. With smartphone adoption and affordable over-the-top content subscriptions accelerating across the Kingdom, cinema operators must continuously reinvest in differentiated experiential formats to justify the in-theatre value proposition. For MENA’s investment community, the Saudi cinema market is thus not merely a bet on screen count growth; it is a nuanced play on the interplay between sovereign industrial policy, consumer behavioral evolution, and the capital discipline required to build a durable entertainment infrastructure layer across a region still in the early innings of its leisure-economy transformation.