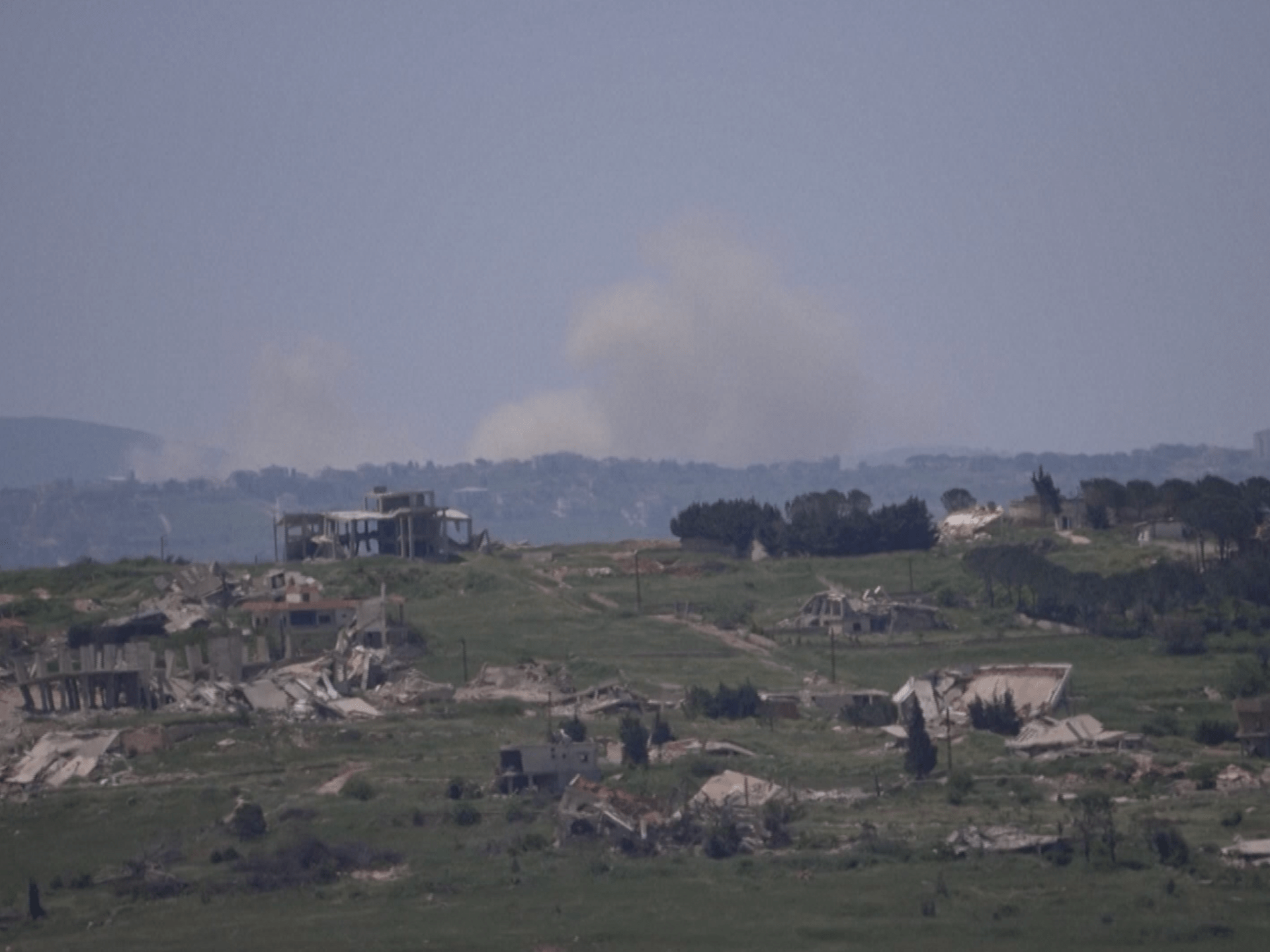

The escalation of hostilities along the Lebanon-Israel frontier represents more than a security concern—it constitutes a material recalibration of risk premiums across the Eastern Mediterranean financial corridor. With critical infrastructure nodes from Beirut port to Tripoli’s emerging logistics hubs now operating under heightened threat assessments, institutional investors are reassessing exposure allocations totaling approximately $12 billion in regional sovereign bond holdings. The conflict’s geographic proximity to Cyprus’s energy export terminals and Egypt’s northern Sinai economic zone has triggered a repricing of regional credit default swaps, with Lebanon’s five-year CDS widening 47 basis points in immediate response. This volatility directly impacts the Gulf Cooperation Council’s $2.3 trillion in combined sovereign wealth assets, as regional funds increasingly factor geopolitical adjacency into their diversification mandates.

Venture capital flows across the Levant face immediate compression as limited partners reassess their emerging market technology allocations. The MENA venture ecosystem, which attracted $3.8 billion in 2025 investments, now confronts a significant de-risking cycle with Lebanon’s startup cluster particularly exposed. Regional venture funds including Mubadala Capital and Saudi Arabia’s Public Investment Fund technology arm have temporarily suspended new Lebanese commitments pending stability assessments. The conflict has accelerated a broader regional consolidation trend, with capital migrating toward perceived safe-haven jurisdictions like Saudi Arabia’s NEOM corridor and Egypt’s new administrative capital, where infrastructure development commitments exceed $85 billion. Early-stage investors are now prioritizing portfolio resilience over growth metrics, fundamentally altering deal structures across the technology sector.

Sovereign infrastructure development strategies across the region are entering a critical reassessment phase, with billions in planned capital expenditure now subject to revised risk models. The World Bank’s $4.7 billion regional infrastructure portfolio requires immediate stress-testing against prolonged instability scenarios, while China’s Belt and Road Initiative faces potential delays in key Lebanese reconstruction contracts valued at $2.1 billion. Gulf sovereign investors, who have committed over $15 billion to regional infrastructure since 2022, are now channeling investments toward less geopolitically-sensitive corridors, particularly Egypt’s Suez Canal Economic Zone and Algeria’s industrial development projects. This redirection of patient capital will likely accelerate the decoupling of regional infrastructure financing from traditional Western-dominated structures toward more Asia-Africa centric partnerships.

The broader macroeconomic implications extend beyond immediate investment flows, potentially reshaping the regional architectural framework that has supported unprecedented capital formation over the past decade. Central banks from Dubai to Rabat are already adjusting liquidity provisions to support counterparty stability, while Islamic banking institutions face increased pressure on Murabaha financing portfolios extended to conflict-affected territories. The longer-term consequence may be an accelerated fragmentation of the unified Gulf-Levant investment thesis that drove unprecedented capital convergence since 2019. Regional exchanges, already witnessing volatility in real estate investment trusts and infrastructure funds, face renewed pressure to develop more sophisticated hedging instruments that can accommodate geopolitical risk premiums historically absent from emerging market sovereign debt calculations.