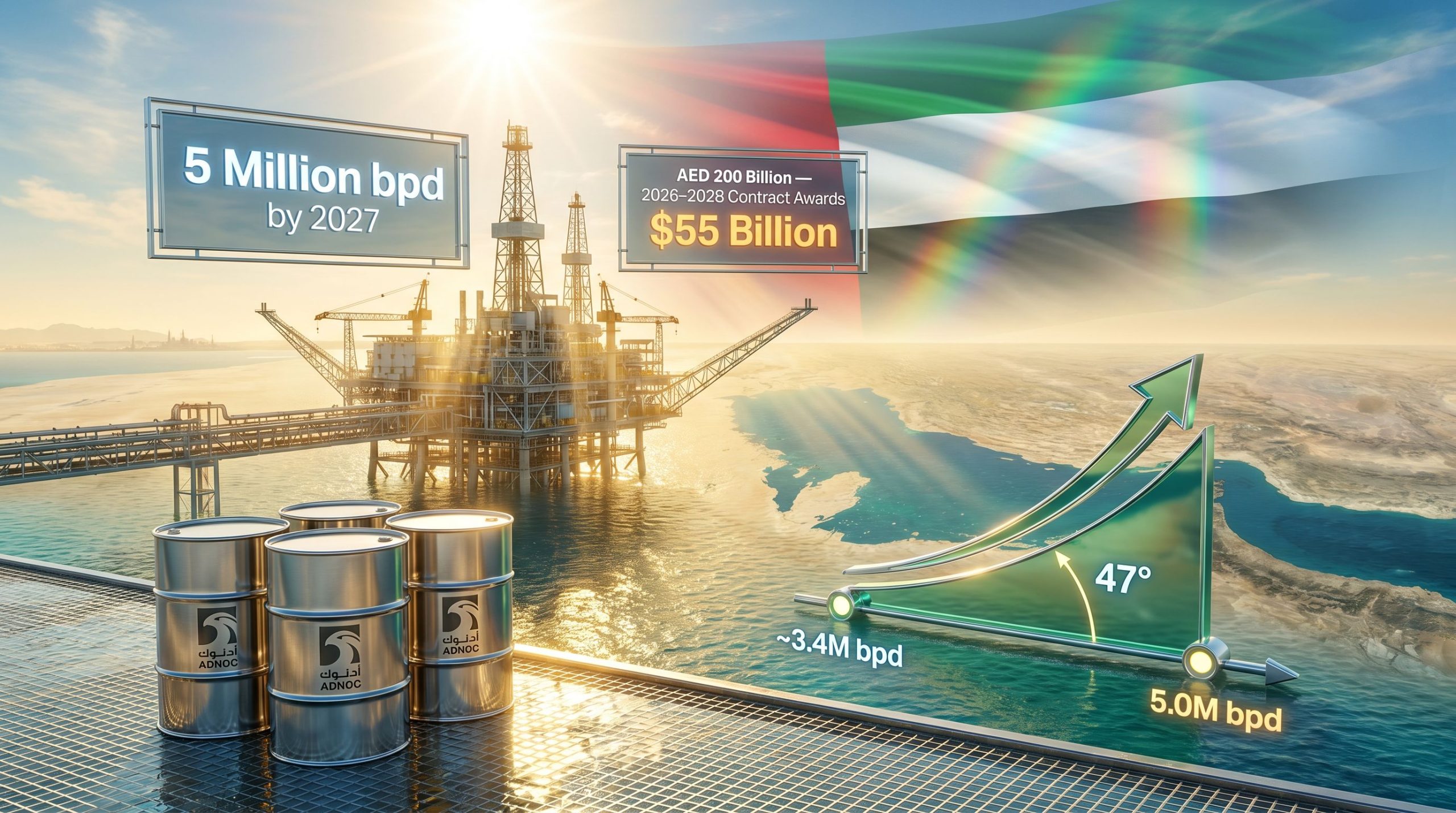

The United Arab Emirates’ formal exit from OPEC on May 1, 2026, following nearly six decades of membership, crystallizes a fundamental shift in Gulf energy geopolitics that carries profound implications for regional sovereign capital deployment and multilateral energy coordination. The decision by Abu Dhabi to prioritize production sovereignty over collective price management reflects a structural calculus that few OPEC members possess: substantial unused productive capacity coupled with fiscal resilience measured at breakeven levels significantly below regional peers. This twin advantage transformed what cartel architects designed as a stabilizing mechanism into a strategic liability, as each restricted barrel represented quantifiable revenue foregone against infrastructure already capitalized. The immediate consequence materialized through ADNOC’s $55 billion acceleration of project awards spanning 2026-2028, representing not new capital but expedited execution of a pre-approved $150 billion five-year programme designed to lift production from 3.4 to 5 million barrels daily by 2027.

Beyond upstream considerations, the UAE’s strategic pivot signals deeper industrial policy ambitions that extend across the MENA region’s evolving economic architecture. ADNOC’s integration of the “Local+” initiative into its capital deployment framework demonstrates how sovereign energy companies can function simultaneously as production vehicles and national development instruments, prioritizing domestic manufacturing and supply chain localization over traditional import-dependent contractor models. This approach challenges conventional OPEC dynamics where hydrocarbon revenues primarily fund external procurement, instead creating multiplier effects that strengthen regional industrial capabilities and reduce technology transfer dependencies. For venture capital investors eyeing MENA’s industrial transformation, the shift indicates growing opportunities in domestic supply chain optimization, advanced materials manufacturing, and energy transition technologies that align with sovereign capacity expansion objectives.

The regional infrastructure implications extend beyond physical export constraints posed by the Strait of Hormuz closure, which currently neutralizes short-term production gains for all Gulf producers regardless of OPEC status. The UAE’s departure creates precedent pressure on other capacity-rich OPEC+ members to reassess their own participation calculus, particularly as Western institutional capital increasingly views OPEC independence as enhancing investment attractiveness and transparency. Saudi Arabia and Iraq, maintaining significant spare capacity within the alliance framework, now face amplified scrutiny regarding their own production potential realization and the credibility of collective output discipline. This dynamic particularly affects regional bond markets and sovereign credit assessments, where production flexibility premiums may begin commanding valuation advantages over coordinated production strategies.

Long-term market architecture implications suggest a gradual migration toward bilateral sovereign-led energy strategies rather than collective cartel coordination, a shift with decade-spanning consequences for pricing mechanisms and geopolitical energy relationships throughout MENA. ADNOC’s positioning represents a calculated bet on medium-to-long-term production advantage once maritime constraints resolve, utilizing current disruption periods for supply chain mobilization and infrastructure advancement rather than immediate market impact. For institutional investors monitoring MENA energy exposure, the convergence of OPEC departure, accelerated capital deployment, and regional conflict creates historically significant inflection points that will likely redefine supply-demand equilibrium assumptions through 2030 and beyond.